Page 26 - Manac Costing Test 2 class slides - 2. Decision Making

P. 26

DECISION MAKING

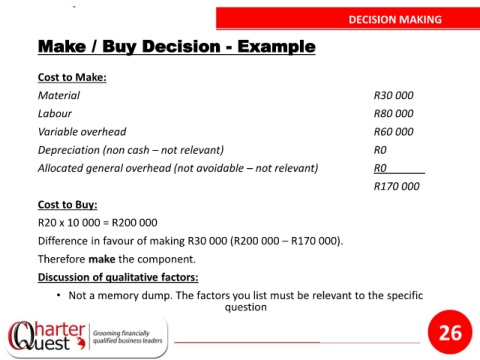

Make / Buy Decision - Example

Cost to Make:

Material R30 000

Labour R80 000

Variable overhead R60 000

Depreciation (non cash – not relevant) R0

Allocated general overhead (not avoidable – not relevant) R0 .

R170 000

Cost to Buy:

R20 x 10 000 = R200 000

Difference in favour of making R30 000 (R200 000 – R170 000).

Therefore make the component.

Discussion of qualitative factors:

• Not a memory dump. The factors you list must be relevant to the specific

question

26