Page 27 - FINAL CFA II SLIDES JUNE 2019 DAY 8

P. 27

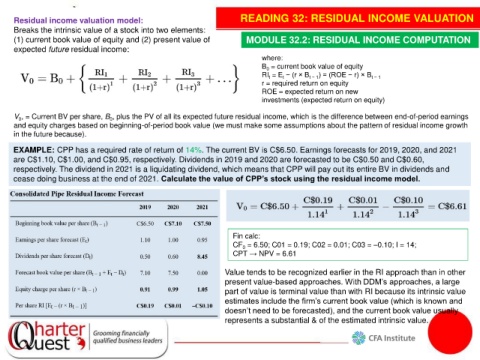

Residual income valuation model: READING 32: RESIDUAL INCOME VALUATION

Breaks the intrinsic value of a stock into two elements:

(1) current book value of equity and (2) present value of MODULE 32.2: RESIDUAL INCOME COMPUTATION

expected future residual income:

where:

B = current book value of equity

0

RI = E − (r × B t − 1 ) = (ROE − r) × B t − 1

t

t

r = required return on equity

ROE = expected return on new

investments (expected return on equity)

V , = Current BV per share, B , plus the PV of all its expected future residual income, which is the difference between end-of-period earnings

0

0

and equity charges based on beginning-of-period book value (we must make some assumptions about the pattern of residual income growth

in the future because).

EXAMPLE: CPP has a required rate of return of 14%. The current BV is C$6.50. Earnings forecasts for 2019, 2020, and 2021

are C$1.10, C$1.00, and C$0.95, respectively. Dividends in 2019 and 2020 are forecasted to be C$0.50 and C$0.60,

respectively. The dividend in 2021 is a liquidating dividend, which means that CPP will pay out its entire BV in dividends and

cease doing business at the end of 2021. Calculate the value of CPP’s stock using the residual income model.

Fin calc:

CF = 6.50; C01 = 0.19; C02 = 0.01; C03 = –0.10; I = 14;

0

CPT → NPV = 6.61

Value tends to be recognized earlier in the RI approach than in other

present value-based approaches. With DDM’s approaches, a large

part of value is terminal value than with RI because its intrinsic value

estimates include the firm’s current book value (which is known and

doesn’t need to be forecasted), and the current book value usually

represents a substantial & of the estimated intrinsic value.