Page 60 - P6 Slide Taxation - Lecture Day 4

P. 60

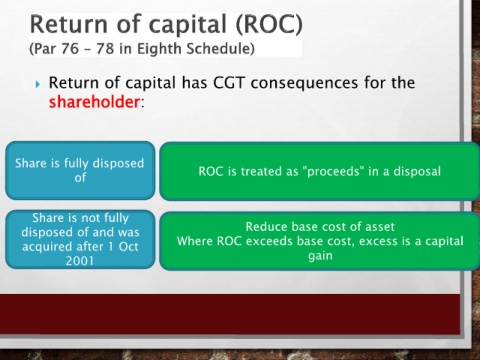

Return of capital has CGT consequences for the

shareholder:

Share is fully disposed

of ROC is treated as "proceeds" in a disposal

Share is not fully

disposed of and was Reduce base cost of asset

acquired after 1 Oct Where ROC exceeds base cost, excess is a capital

2001 gain