Page 9 - P6 Slide Taxation - Lecture Day 4

P. 9

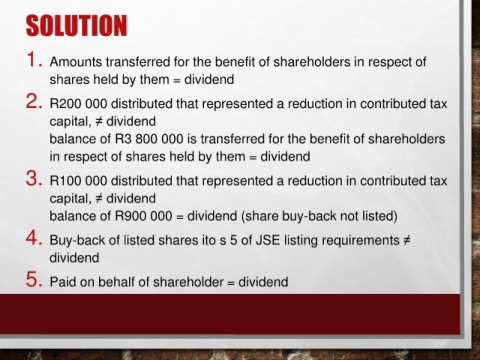

SOLUTION

1. Amounts transferred for the benefit of shareholders in respect of

shares held by them = dividend

2. R200 000 distributed that represented a reduction in contributed tax

capital, ≠ dividend

balance of R3 800 000 is transferred for the benefit of shareholders

in respect of shares held by them = dividend

3. R100 000 distributed that represented a reduction in contributed tax

capital, ≠ dividend

balance of R900 000 = dividend (share buy-back not listed)

4. Buy-back of listed shares ito s 5 of JSE listing requirements ≠

dividend

5. Paid on behalf of shareholder = dividend