Page 335 - SBR Integrated Workbook STUDENT S18-J19

P. 335

Group statement of cash flows

Consolidated cash flows

3.1 Introduction

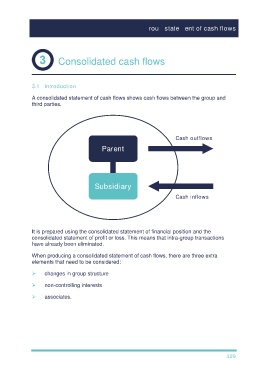

A consolidated statement of cash flows shows cash flows between the group and

third parties.

Cash outflows

Parent

Subsidiary

Cash inflows

It is prepared using the consolidated statement of financial position and the

consolidated statement of profit or loss. This means that intra-group transactions

have already been eliminated.

When producing a consolidated statement of cash flows, there are three extra

elements that need to be considered:

changes in group structure

non-controlling interests

associates.

329