Page 67 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 67

International Taxation

Types of foreign tax

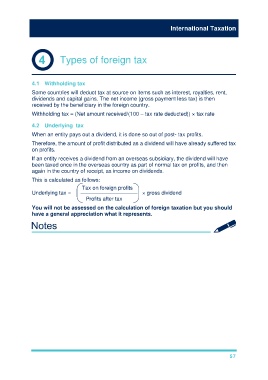

4.1 Withholding tax

Some countries will deduct tax at source on items such as interest, royalties, rent,

dividends and capital gains. The net income (gross payment less tax) is then

received by the beneficiary in the foreign country.

Withholding tax = (Net amount received/(100 – tax rate deducted)) × tax rate

4.2 Underlying tax

When an entity pays out a dividend, it is done so out of post- tax profits.

Therefore, the amount of profit distributed as a dividend will have already suffered tax

on profits.

If an entity receives a dividend from an overseas subsidiary, the dividend will have

been taxed once in the overseas country as part of normal tax on profits, and then

again in the country of receipt, as income on dividends.

This is calculated as follows:

Tax on foreign profits

Underlying tax = ––––––––––––––––––– × gross dividend

Profits after tax

You will not be assessed on the calculation of foreign taxation but you should

have a general appreciation what it represents.

57