Page 260 - F2 Integrated Workbook STUDENT 2019

P. 260

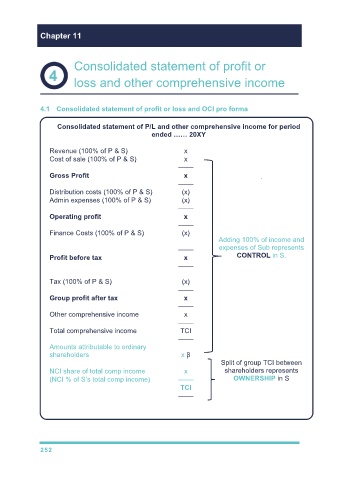

Chapter 11

Consolidated statement of profit or

loss and other comprehensive income

4.1 Consolidated statement of profit or loss and OCI pro forma

Consolidated statement of P/L and other comprehensive income for period

ended …… 20XY

Revenue (100% of P & S) x

Cost of sale (100% of P & S) x

––––

Gross Profit x .

––––

Distribution costs (100% of P & S) (x)

Admin expenses (100% of P & S) (x)

––––

Operating profit x

––––

Finance Costs (100% of P & S) (x)

Adding 100% of income and

–––– expenses of Sub represents

Profit before tax x CONTROL in S.

––––

Tax (100% of P & S) (x)

––––

Group profit after tax x

––––

Other comprehensive income x

––––

Total comprehensive income TCI

––––

Amounts attributable to ordinary

shareholders x β

Split of group TCI between

NCI share of total comp income x shareholders represents

(NCI % of S’s total comp income) –––– OWNERSHIP in S

TCI

––––

252