Page 325 - F2 Integrated Workbook STUDENT 2019

P. 325

Changes in group structure

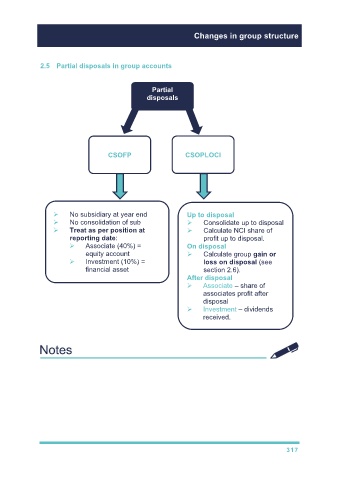

2.5 Partial disposals in group accounts

Partial

disposals

Non-control to CSOPLOCI

CSOFP

control

No subsidiary at year end Up to disposal

No consolidation of sub Consolidate up to disposal

Treat as per position at Calculate NCI share of

reporting date: profit up to disposal.

Associate (40%) = On disposal

equity account Calculate group gain or

Investment (10%) = loss on disposal (see

financial asset section 2.6).

After disposal

Associate – share of

associates profit after

disposal

Investment – dividends

received.

317