Page 217 - F3 -FA Integrated Workbook STUDENT 2018-19

P. 217

The trial balance, accounting errors and suspense accounts

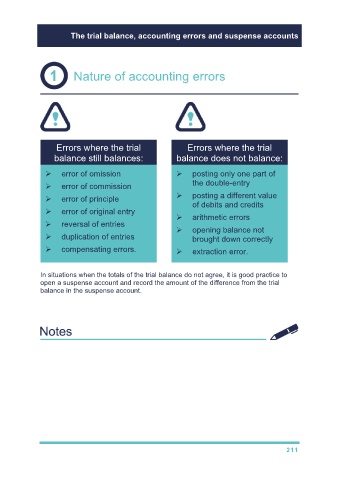

Nature of accounting errors

Errors where the trial Errors where the trial

balance still balances: balance does not balance:

error of omission posting only one part of

error of commission the double-entry

error of principle posting a different value

of debits and credits

error of original entry

arithmetic errors

reversal of entries

opening balance not

duplication of entries brought down correctly

compensating errors. extraction error.

In situations when the totals of the trial balance do not agree, it is good practice to

open a suspense account and record the amount of the difference from the trial

balance in the suspense account.

The use of a suspense account allows financial statements to be prepared subject to

the correction of errors.

211