Page 31 - Trading Stock

P. 31

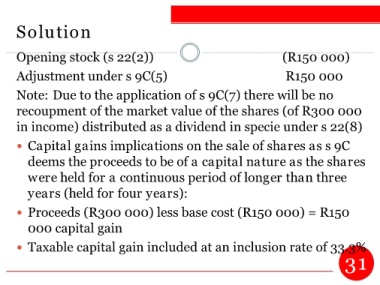

Solution

Opening stock (s 22(2)) (R150 000)

Adjustment under s 9C(5) R150 000

Note: Due to the application of s 9C(7) there will be no

recoupment of the market value of the shares (of R300 000

in income) distributed as a dividend in specie under s 22(8)

Capital gains implications on the sale of shares as s 9C

deems the proceeds to be of a capital nature as the shares

were held for a continuous period of longer than three

years (held for four years):

Proceeds (R300 000) less base cost (R150 000) = R150

000 capital gain

Taxable capital gain included at an inclusion rate of 33.3%

31