Page 173 - Microsoft Word - 00 P1 IW Prelims.docx

P. 173

Reporting

The independent auditor’s report

1.1 Objectives of an auditor

The objectives of an auditor, in accordance with ISA 700 (Revised) Forming an

Opinion and Reporting on Financial Statements, are:

to form an opinion on the financial statements based upon an evaluation of their

conclusions drawn from audit evidence.

to express clearly that opinion through a written report.

When the auditor concludes that the financial statements are prepared, in all material

respects, in accordance with the applicable financial reporting framework, i.e. give a

true and fair view, they issue an unmodified opinion.

If there are no other matters which the auditor wishes to draw to the attention of the

users, they will issue an unmodified report.

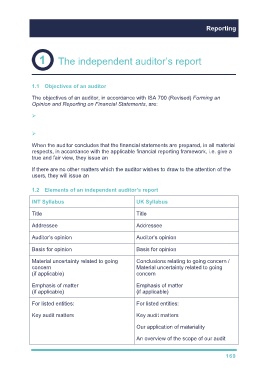

1.2 Elements of an independent auditor’s report

INT Syllabus UK Syllabus

Title Title

Addressee Addressee

Auditor’s opinion Auditor’s opinion

Basis for opinion Basis for opinion

Material uncertainty related to going Conclusions relating to going concern /

concern Material uncertainty related to going

(if applicable) concern

Emphasis of matter Emphasis of matter

(if applicable) (if applicable)

For listed entities: For listed entities:

Key audit matters Key audit matters

Our application of materiality

An overview of the scope of our audit

169