Page 23 - PM Integrated Workbook 2018-19

P. 23

A revision of Management Accounting (MA) topics

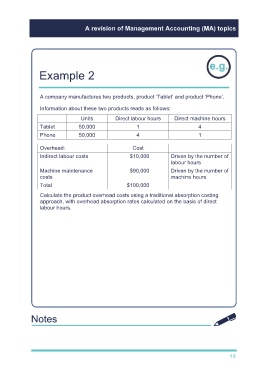

Example 2

A company manufactures two products, product ‘Tablet’ and product ‘Phone’.

Information about these two products reads as follows:

Units Direct labour hours Direct machine hours

Tablet 50,000 1 4

Phone 50,000 4 1

Overhead: Cost

Indirect labour costs $10,000 Driven by the number of

labour hours

Machine maintenance $90,000 Driven by the number of

costs machine hours

Total $100,000

Calculate the product overhead costs using a traditional absorption costing

approach, with overhead absorption rates calculated on the basis of direct

labour hours.

Using a traditional absorption costing approach, the OAR may be calculated

for each production cost centre as total overheads divided by total labour

hours:

$100,000

OAR =

{ 1 × 50,000 + 4 × 50,000 }

OAR = $0.40 per labour hour.

Under traditional absorption costing, overheads would be absorbed into the

two products as follows:

Overheads absorbed into product ‘Tablet’: 1 hour × $0.40 = $0.40

Overheads absorbed into product ‘Phone’: 4 hours × $0.40 = $1.60

15