Page 78 - Microsoft Word - 00 Prelims.docx

P. 78

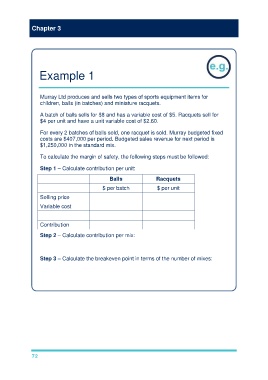

Chapter 3

Example 1

Murray Ltd produces and sells two types of sports equipment items for

children, balls (in batches) and miniature racquets.

A batch of balls sells for $8 and has a variable cost of $5. Racquets sell for

$4 per unit and have a unit variable cost of $2.60.

For every 2 batches of balls sold, one racquet is sold. Murray budgeted fixed

costs are $407,000 per period. Budgeted sales revenue for next period is

$1,250,000 in the standard mix.

To calculate the margin of safety, the following steps must be followed:

Step 1 – Calculate contribution per unit:

Balls Racquets

$ per batch $ per unit

Selling price $8 $4

Variable cost $5 $2.60

–––– –––––

Contribution $3 $1.40

Step 2 – Calculate contribution per mix:

($3 × 2 batches) + ($1.40 × 1 racquet) = $7.40

Step 3 – Calculate the breakeven point in terms of the number of mixes:

Breakeven point = Fixed costs/Contribution per mix

Breakeven point = $407,000/$7.40 = 55,000 mixes

72