Page 58 - AA Integrated Workbook STUDENT 2018-19

P. 58

Chapter 5 3

Materiality

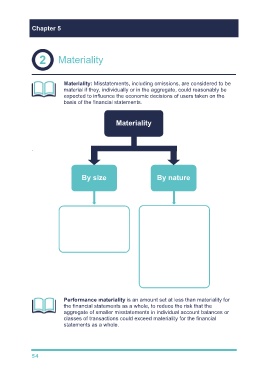

Materiality: Misstatements, including omissions, are considered to be

material if they, individually or in the aggregate, could reasonably be

expected to influence the economic decisions of users taken on the

basis of the financial statements.

Materiality

.

By size By nature

½ – 1 % Revenue Compliance with

laws and

5 – 10% Profit regulations

1 – 2 % Total Compliance with

assets debt covenants

Turn a profit to a

loss

Transactions with

directors

Performance materiality is an amount set at less than materiality for

the financial statements as a whole, to reduce the risk that the

aggregate of smaller misstatements in individual account balances or

classes of transactions could exceed materiality for the financial

statements as a whole.

54