Page 75 - AA Integrated Workbook STUDENT 2018-19

P. 75

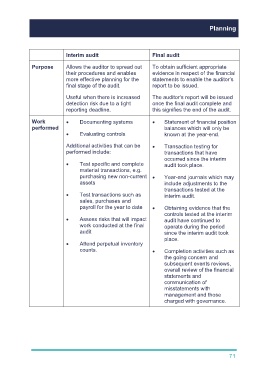

Planning

Interim audit Final audit

Purpose Allows the auditor to spread out To obtain sufficient appropriate

their procedures and enables evidence in respect of the financial

more effective planning for the statements to enable the auditor’s

final stage of the audit. report to be issued.

Useful when there is increased The auditor’s report will be issued

detection risk due to a tight once the final audit complete and

reporting deadline. this signifies the end of the audit.

Work Documenting systems Statement of financial position

performed balances which will only be

Evaluating controls known at the year-end.

Additional activities that can be Transaction testing for

performed include: transactions that have

occurred since the interim

Test specific and complete audit took place.

material transactions, e.g.

purchasing new non-current Year-end journals which may

assets include adjustments to the

transactions tested at the

Test transactions such as interim audit.

sales, purchases and

payroll for the year to date Obtaining evidence that the

controls tested at the interim

Assess risks that will impact audit have continued to

work conducted at the final operate during the period

audit since the interim audit took

place.

Attend perpetual inventory

counts. Completion activities such as

the going concern and

subsequent events reviews,

overall review of the financial

statements and

communication of

misstatements with

management and those

charged with governance.

71