Page 57 - Unisa Test 4 Manac Slides

P. 57

DECISION MAKING

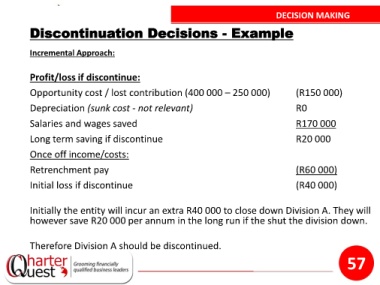

Discontinuation Decisions - Example

Incremental Approach:

Profit/loss if discontinue:

Opportunity cost / lost contribution (400 000 – 250 000) (R150 000)

Depreciation (sunk cost - not relevant) R0

Salaries and wages saved R170 000

Long term saving if discontinue R20 000

Once off income/costs:

Retrenchment pay (R60 000)

Initial loss if discontinue (R40 000)

Initially the entity will incur an extra R40 000 to close down Division A. They will

however save R20 000 per annum in the long run if the shut the division down.

Therefore Division A should be discontinued.

57