Page 345 - F1 Integrated Workbook STUDENT 2018

P. 345

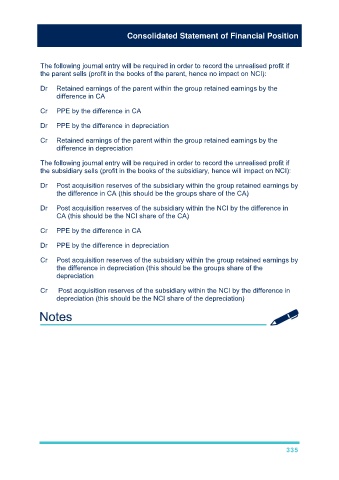

Consolidated Statement of Financial Position

The following journal entry will be required in order to record the unrealised profit if

the parent sells (profit in the books of the parent, hence no impact on NCI):

Dr Retained earnings of the parent within the group retained earnings by the

difference in CA

Cr PPE by the difference in CA

Dr PPE by the difference in depreciation

Cr Retained earnings of the parent within the group retained earnings by the

difference in depreciation

The following journal entry will be required in order to record the unrealised profit if

the subsidiary sells (profit in the books of the subsidiary, hence will impact on NCI):

Dr Post acquisition reserves of the subsidiary within the group retained earnings by

the difference in CA (this should be the groups share of the CA)

Dr Post acquisition reserves of the subsidiary within the NCI by the difference in

CA (this should be the NCI share of the CA)

Cr PPE by the difference in CA

Dr PPE by the difference in depreciation

Cr Post acquisition reserves of the subsidiary within the group retained earnings by

the difference in depreciation (this should be the groups share of the

depreciation

Cr Post acquisition reserves of the subsidiary within the NCI by the difference in

depreciation (this should be the NCI share of the depreciation)

335