Page 367 - F1 Integrated Workbook STUDENT 2018

P. 367

Associates

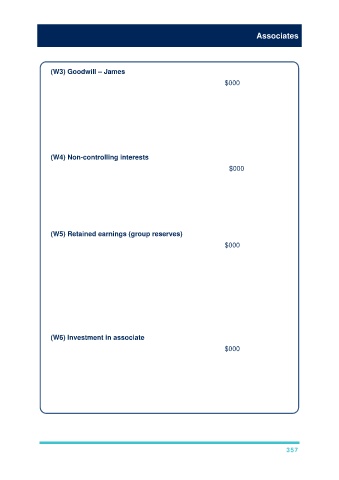

(W3) Goodwill – James

$000

Fair value of investment 805.0

NCI at acquisition 25% × 784 (W2) 196

Fair value of net assets acquired

100% × 784 (W2) (784.0)

———

Goodwill 217.0

———

(W4) Non-controlling interests

$000

Value of NCI at acquisition (W3) 196.0

NCI × post-acquisition reserves 25% × (1,442 – 784) (W2) 164.5

NCI × impairment (W3) (fair value method only) –

–––––

NCI at reporting date 360.5

–––––

(W5) Retained earnings (group reserves)

$000

Tom 1,232.0

James – share of post-acquisition reserves

(75% × (1,442 – 784)) (W2) 493.5

Emily – share of post-acquisition reserves

(30% × (1,008 – 700)) (W2) 92.4

Less: impairments to date (2.8)

–––––––

1,815.1

–––––––

(W6) Investment in associate

$000

Fair value of investment 224.0

Share of post-acquisition profits (W5) 92.4

Less: impairment (2.8)

––––––

313.6

––––––

357