Page 130 - P6 Slide Taxation - Lecture Day 5 - VAT Part 1

P. 130

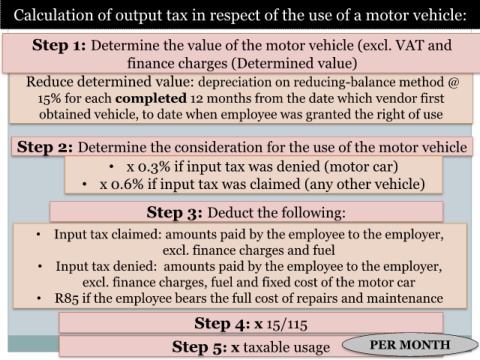

Calculation of output tax in respect of the use of a motor vehicle:

Step 1: Determine the value of the motor vehicle (excl. VAT and

finance charges (Determined value)

Reduce determined value: depreciation on reducing-balance method @

15% for each completed 12 months from the date which vendor first

obtained vehicle, to date when employee was granted the right of use

Step 2: Determine the consideration for the use of the motor vehicle

• x 0.3% if input tax was denied (motor car)

• x 0.6% if input tax was claimed (any other vehicle)

Step 3: Deduct the following:

• Input tax claimed: amounts paid by the employee to the employer,

excl. finance charges and fuel

• Input tax denied: amounts paid by the employee to the employer,

excl. finance charges, fuel and fixed cost of the motor car

• R85 if the employee bears the full cost of repairs and maintenance

Step 4: x 15/115

Step 5: x taxable usage PER MONTH