Page 59 - PowerPoint Presentation

P. 59

CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS

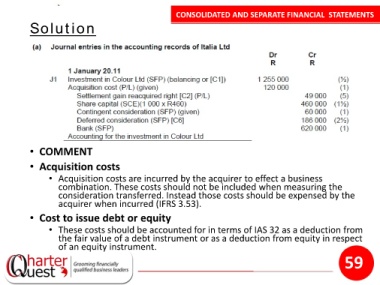

Solution

• COMMENT

• Acquisition costs

• Acquisition costs are incurred by the acquirer to effect a business

combination. These costs should not be included when measuring the

consideration transferred. Instead those costs should be expensed by the

acquirer when incurred (IFRS 3.53).

• Cost to issue debt or equity

• These costs should be accounted for in terms of IAS 32 as a deduction from

the fair value of a debt instrument or as a deduction from equity in respect

of an equity instrument.

59