Page 26 - P6 Slide Taxation - Lecture Day 6 - Retirement Benefits Lump Sums

P. 26

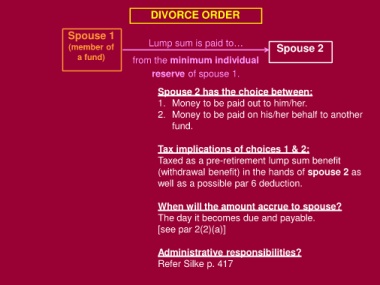

DIVORCE ORDER

Spouse 1

(member of Lump sum is paid to… Spouse 2

a fund) from the minimum individual

reserve of spouse 1.

Spouse 2 has the choice between:

1. Money to be paid out to him/her.

2. Money to be paid on his/her behalf to another

fund.

Tax implications of choices 1 & 2:

Taxed as a pre-retirement lump sum benefit

(withdrawal benefit) in the hands of spouse 2 as

well as a possible par 6 deduction.

When will the amount accrue to spouse?

The day it becomes due and payable.

[see par 2(2)(a)]

Administrative responsibilities?

Refer Silke p. 417