Page 14 - FAC4862_4 Topic 2 slides cm

P. 14

INVESTMENTS IN ASSOCIATES AND JOINT VENTURES

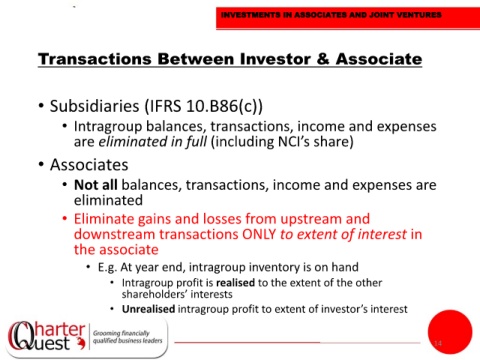

Transactions Between Investor & Associate

• Subsidiaries (IFRS 10.B86(c))

• Intragroup balances, transactions, income and expenses

are eliminated in full (including NCI’s share)

• Associates

• Not all balances, transactions, income and expenses are

eliminated

• Eliminate gains and losses from upstream and

downstream transactions ONLY to extent of interest in

the associate

• E.g. At year end, intragroup inventory is on hand

• Intragroup profit is realised to the extent of the other

shareholders’ interests

• Unrealised intragroup profit to extent of investor’s interest

14