Page 156 - Policy Wording - Hollard Business Binder (2020-08-26)

P. 156

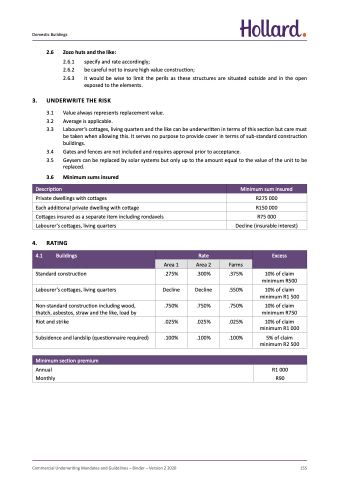

Domestic Buildings

2.6 Zozo huts and the like:

2.6.1 specify and rate accordingly;

2.6.2 be careful not to insure high value construction;

2.6.3 it would be wise to limit the perils as these structures are situated outside and in the open exposed to the elements.

3. UNDERWRITE THE RISK

3.1 Value always represents replacement value.

3.2 Average is applicable.

3.3 Labourer’s cottages, living quarters and the like can be underwritten in terms of this section but care must be taken when allowing this. It serves no purpose to provide cover in terms of sub-standard construction buildings.

3.4 Gates and fences are not included and requires approval prior to acceptance.

3.5 Geysers can be replaced by solar systems but only up to the amount equal to the value of the unit to be replaced.

3.6 Minimum sums insured

Private dwellings with cottages

Each additional private dwelling with cottage

Cottages insured as a separate item including rondavels Labourer’s cottages, living quarters

R275 000

R150 000

R75 000

Decline (insurable interest)

Description

Minimum sum insured

4. RATING

Standard construction

Labourer’s cottages, living quarters

Non-standard construction including wood, thatch, asbestos, straw and the like, load by

Riot and strike

Subsidence and landslip (questionnaire required)

Minimum section premium

Annual Monthly

.275%

Decline

.750%

.025%

.100%

.300%

Decline

.750%

.025%

.100%

.375%

.550%

.750%

.025%

.100%

10% of claim minimum R500

10% of claim minimum R1 500

10% of claim minimum R750

10% of claim minimum R1 000

5% of claim minimum R2 500

R1 000 R90

4.1 Buildings

Rate

Excess

Area 1

Area 2

Farms

Commercial Underwriting Mandates and Guidelines – Binder – Version 2 2020

155