Page 34 - How To Refi Cashout Your Commercial Property Before The Bank Says...

P. 34

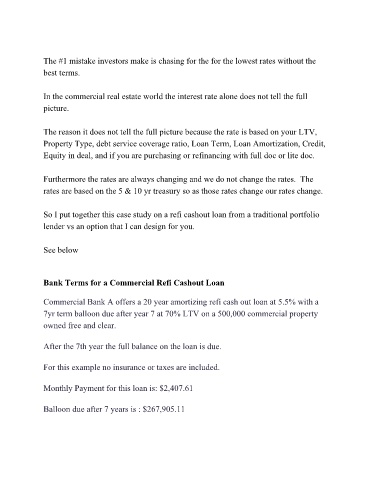

The #1 mistake investors make is chasing for the for the lowest rates without the

best terms.

In the commercial real estate world the interest rate alone does not tell the full

picture.

The reason it does not tell the full picture because the rate is based on your LTV,

Property Type, debt service coverage ratio, Loan Term, Loan Amortization, Credit,

Equity in deal, and if you are purchasing or refinancing with full doc or lite doc.

Furthermore the rates are always changing and we do not change the rates. The

rates are based on the 5 & 10 yr treasury so as those rates change our rates change.

So I put together this case study on a refi cashout loan from a traditional portfolio

lender vs an option that I can design for you.

See below

Bank Terms for a Commercial Refi Cashout Loan

Commercial Bank A offers a 20 year amortizing refi cash out loan at 5.5% with a

7yr term balloon due after year 7 at 70% LTV on a 500,000 commercial property

owned free and clear.

After the 7th year the full balance on the loan is due.

For this example no insurance or taxes are included.

Monthly Payment for this loan is: $2,407.61

Balloon due after 7 years is : $267,905.11