Page 190 - JoFA_2022

P. 190

AUDITING

The Code is the only

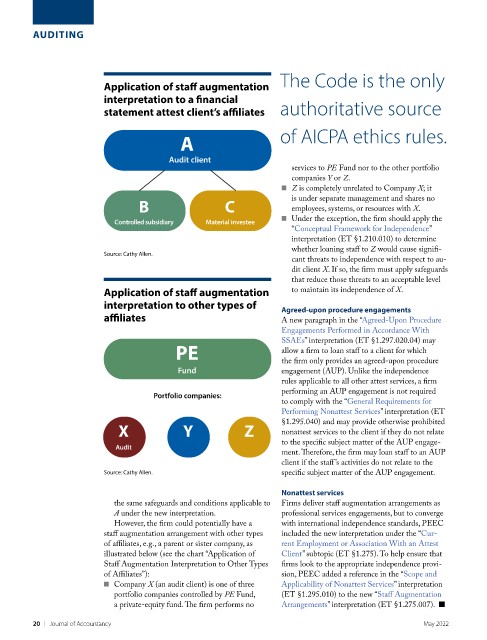

Application of staff augmentation

interpretation to a financial

statement attest client’s affiliates authoritative source

A of AICPA ethics rules.

Audit client

services to PE Fund nor to the other portfolio

companies Y or Z.

■

Z is completely unrelated to Company X; it

B C is under separate management and shares no

employees, systems, or resources with X.

Controlled subsidiary Material investee ■ Under the exception, the firm should apply the

“Conceptual Framework for Independence”

interpretation (ET §1.210.010) to determine

whether loaning staff to Z would cause signifi-

Source: Cathy Allen.

cant threats to independence with respect to au-

dit client X. If so, the firm must apply safeguards

that reduce those threats to an acceptable level

Application of staff augmentation to maintain its independence of X.

interpretation to other types of Agreed-upon procedure engagements

affiliates A new paragraph in the “Agreed-Upon Procedure

Engagements Performed in Accordance With

PE SSAEs” interpretation (ET §1.297.020.04) may

allow a firm to loan staff to a client for which

the firm only provides an agreed-upon procedure

Fund engagement (AUP). Unlike the independence

rules applicable to all other attest services, a firm

Portfolio companies: performing an AUP engagement is not required

to comply with the “General Requirements for

Performing Nonattest Services” interpretation (ET

X Y Z §1.295.040) and may provide otherwise prohibited

nonattest services to the client if they do not relate

to the specific subject matter of the AUP engage-

Audit

ment. Therefore, the firm may loan staff to an AUP

client if the staff ’s activities do not relate to the

Source: Cathy Allen. specific subject matter of the AUP engagement.

Nonattest services

the same safeguards and conditions applicable to Firms deliver staff augmentation arrangements as

A under the new interpretation. professional services engagements, but to converge

However, the firm could potentially have a with international independence standards, PEEC

staff augmentation arrangement with other types included the new interpretation under the “Cur-

of affiliates, e.g., a parent or sister company, as rent Employment or Association With an Attest

illustrated below (see the chart “Application of Client” subtopic (ET §1.275). To help ensure that

Staff Augmentation Interpretation to Other Types firms look to the appropriate independence provi-

of Affiliates”): sion, PEEC added a reference in the “Scope and

■ Company X (an audit client) is one of three Applicability of Nonattest Services” interpretation

portfolio companies controlled by PE Fund, (ET §1.295.010) to the new “Staff Augmentation

a private-equity fund. The firm performs no Arrangements” interpretation (ET §1.275.007). ■

20 | Journal of Accountancy May 2022