Page 391 - Auditing Standards

P. 391

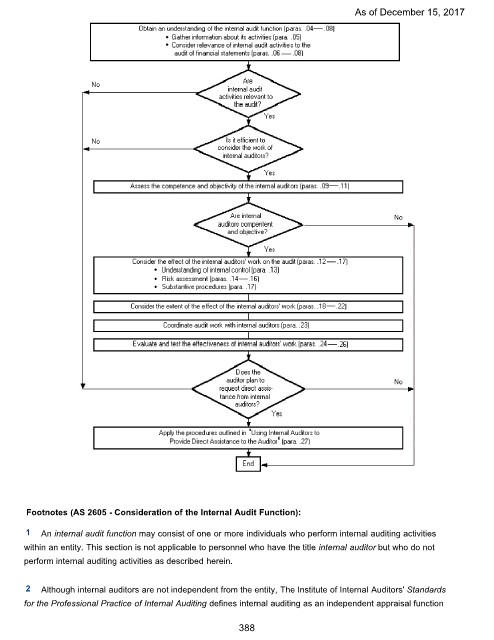

As of December 15, 2017

Footnotes (AS 2605 - Consideration of the Internal Audit Function):

1 An internal audit function may consist of one or more individuals who perform internal auditing activities

within an entity. This section is not applicable to personnel who have the title internal auditor but who do not

perform internal auditing activities as described herein.

2 Although internal auditors are not independent from the entity, The Institute of Internal Auditors' Standards

for the Professional Practice of Internal Auditing defines internal auditing as an independent appraisal function

388