Page 648 - Auditing Standards

P. 648

As of December 15, 2017

Had we performed additional procedures or had we made an examination of the forecast in accordance

with the standards of the Public Company Accounting Oversight Board, matters might have come to our

attention that would have been reported to you. Furthermore, there will usually be differences between the

forecasted and actual results, because events and circumstances frequently do not occur as expected,

and those differences may be material.

Example F: Comments on Tables, Statistics, and Other Financial Information—

Complete Description of Procedures and Findings

7. Example F is applicable when the accountants are asked to comment on tables, statistics, or other

compilations of information appearing in a registration statement (paragraphs .54 through .60). Each of the

comments is in response to a specific request. The paragraphs in example F are intended to follow paragraph

6 in example A.

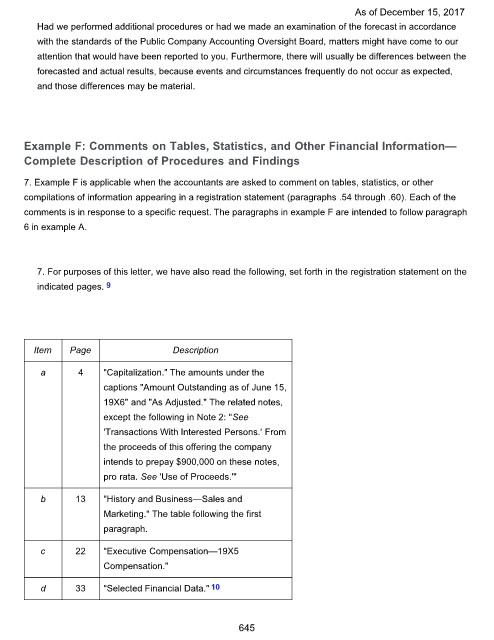

7. For purposes of this letter, we have also read the following, set forth in the registration statement on the

indicated pages. 9

Item Page Description

a 4 "Capitalization." The amounts under the

captions "Amount Outstanding as of June 15,

19X6" and "As Adjusted." The related notes,

except the following in Note 2: "See

'Transactions With Interested Persons.' From

the proceeds of this offering the company

intends to prepay $900,000 on these notes,

pro rata. See 'Use of Proceeds.'"

b 13 "History and Business—Sales and

Marketing." The table following the first

paragraph.

c 22 "Executive Compensation—19X5

Compensation."

d 33 "Selected Financial Data." 10

645