Page 669 - ACFE Fraud Reports 2009_2020

P. 669

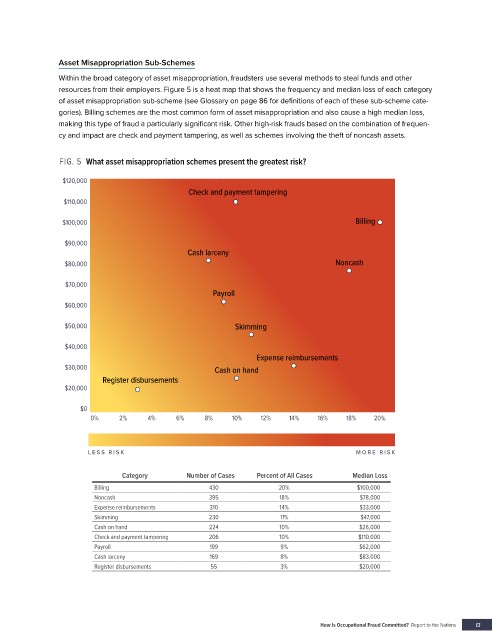

Asset Misappropriation Sub-Schemes

Within the broad category of asset misappropriation, fraudsters use several methods to steal funds and other

resources from their employers. Figure 5 is a heat map that shows the frequency and median loss of each category

of asset misappropriation sub-scheme (see Glossary on page 86 for definitions of each of these sub-scheme cate-

gories). Billing schemes are the most common form of asset misappropriation and also cause a high median loss,

making this type of fraud a particularly significant risk. Other high-risk frauds based on the combination of frequen-

cy and impact are check and payment tampering, as well as schemes involving the theft of noncash assets.

FIG. 5 What asset misappropriation schemes present the greatest risk?

$120,000

Check and payment tampering

$110,000

$100,000 Billing

$90,000

Cash larceny

$80,000 Noncash

$70,000

Payroll

$60,000

$50,000 Skimming

$40,000

Expense reimbursements

$30,000 Cash on hand

Register disbursements

$20,000

$0

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

LESS RISK MORE RISK

Category Number of Cases Percent of All Cases Median Loss

Billing 430 20% $100,000

Noncash 395 18% $78,000

Expense reimbursements 310 14% $33,000

Skimming 230 11% $47,000

Cash on hand 224 10% $26,000

Check and payment tampering 206 10% $110,000

Payroll 199 9% $62,000

Cash larceny 169 8% $83,000

Register disbursements 55 3% $20,000

R

eport to the Nations

How Is Occupational Fraud Committed?

How Is Occupational Fraud Committed? Report to the Nations 13