Page 33 - Daphne Axton AZHG

P. 33

WAYS TO TAKE TITLE IN

Photograph by: Desha Jackson (Tucson River)

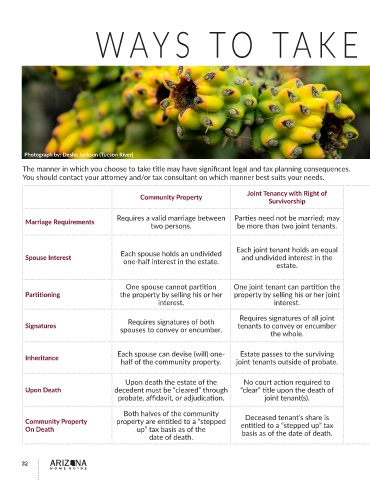

The manner in which you choose to take title may have significant legal and tax planning consequences.

You should contact your attorney and/or tax consultant on which manner best suits your needs.

Community Property Joint Tenancy with Right of Community Property with Right of Tenancy in Common

Survivorship Survivorship

Requires a valid marriage between Parties need not be married; may Requires a valid marriage Parties need not be married; may be

Marriage Requirements

two persons. be more than two joint tenants. between two persons. more than two tenants in common.

Each tenant in common holds an

Each joint tenant holds an equal undivided and fractional interest in

Each spouse holds an undivided Each spouse holds an undivided

Spouse Interest and undivided interest in the the estate. Can be disproportionate,

one-half interest in the estate. estate. one-half interest in the estate. i.e. 20% & 80%; 60% & 40%; 20%,

20%, 20%, & 40%; etc.

One spouse cannot partition One joint tenant can partition the One spouse cannot partition Each tenant’s share can be

Partitioning the property by selling his or her property by selling his or her joint the property by selling his or conveyed, encumbered or devised

interest. interest. her interest. to a third party.

Requires signatures of both Requires signatures of all joint Requires signatures of both Requires signatures of all tenants to

Signatures spouses to convey or encumber. tenants to convey or encumber spouses to convey or encumber. convey or encumber the whole.

the whole.

Each spouse can devise (will) one- Estate passes to the surviving Estate passes to the surviving Upon death the tenant’s

Inheritance proportionate share passes to heirs

half of the community property. joint tenants outside of probate. spouse outside of probate.

by will or intestacy.

Upon death the estate of the No court action required to No court action required to Upon death the estate of the

Upon Death decedent must be “cleared” through “clear” title upon the death of “clear” title upon the first death. decedent must be “cleared” through

probate, affidavit, or adjudication. joint tenant(s). probate, affidavit, or adjudication.

Both halves of the community Deceased tenant’s share is Both halves of the community

Community Property property are entitled to a “stepped entitled to a “stepped up” tax property are entitled to a Each share has its own tax basis.

On Death up” tax basis as of the basis as of the date of death. “stepped up” tax.

date of death.

32 ARIZ NA

HOME GUIDE