Page 39 - Cost Accounting - Ready Reckoner

P. 39

36

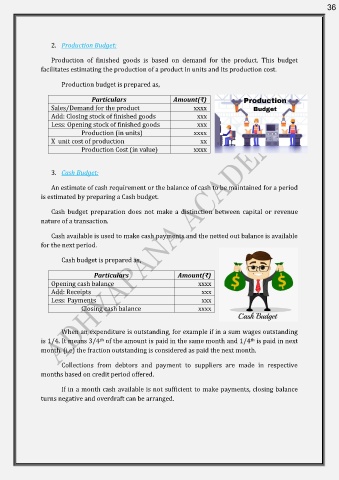

2. Production Budget:

Production of finished goods is based on demand for the product. This budget

facilitates estimating the production of a product in units and its production cost.

Production budget is prepared as,

Particulars Amount(₹)

Sales/Demand for the product xxxx

Add: Closing stock of finished goods xxx

Less: Opening stock of finished goods xxx

Production (in units) xxxx

X unit cost of production xx

Production Cost (in value) xxxx

3. Cash Budget:

An estimate of cash requirement or the balance of cash to be maintained for a period

is estimated by preparing a Cash budget.

Cash budget preparation does not make a distinction between capital or revenue

nature of a transaction.

Cash available is used to make cash payments and the netted out balance is available

for the next period.

Cash budget is prepared as,

Particulars Amount(₹)

Opening cash balance xxxx

Add: Receipts xxx

Less: Payments xxx

Closing cash balance xxxx

When an expenditure is outstanding, for example if in a sum wages outstanding

is 1/4. It means 3/4 of the amount is paid in the same month and 1/4 is paid in next

th

th

month. (i.e) the fraction outstanding is considered as paid the next month.

Collections from debtors and payment to suppliers are made in respective

months based on credit period offered.

If in a month cash available is not sufficient to make payments, closing balance

turns negative and overdraft can be arranged.