Page 121 - W01TB8_2017-18_[low-res]_F2F_Neat

P. 121

Chapter 8 Contribution and subrogation 8/5

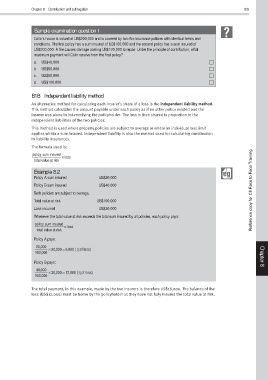

Sample examination question 1

Colin’s house is valued at US$200,000 and is covered by two fire insurance policies with identical terms and

conditions. The first policy has a sum insured of US$100,000 and the second policy has a sum insured of

US$200,000. A fire causes damage costing US$120,000 to repair. Under the principle of contribution, what

maximum payment will Colin receive from the first policy?

a. US$40,000. F

b. US$50,000. F

c. US$60,000. F

d. US$100,000. F

B1B Independent liability method

An alternative method for calculating each insurer’s share of a loss is the independent liability method.

This method calculates the amount payable under each policy as if no other policy existed and the

insurer was alone in indemnifying the policyholder. The loss is then shared in proportion to the

independent liabilities of the two policies.

This method is used where property policies are subject to average or where an individual loss limit

applies within a sum insured. Independent liability is also the method used for calculating contribution

in liability insurances.

The formula used is:

policy sum insured × loss

total value at risk

Example 8.2

Policy A sum insured US$20,000

Policy B sum insured US$40,000

Both policies are subject to average. Reference copy for CII Face to Face Training

Total value at risk US$100,000

Loss incurred US$30,000

Whenever the total value at risk exceeds the total sum insured by all policies, each policy pays:

policy sum insured × loss

total value at risk

Policy A pays:

20,000

=

1

× 30,000 6,000 ( of loss)

5

100,000 Chapter

Policy B pays: 8

40,000

=

× 30,000 12,000 ( of loss)

2

5

100,000

The total payment, in this example, made by the two insurers is therefore US$18,000. The balance of the

loss (US$12,000) must be borne by the policyholder as they have not fully insured the total value at risk.