Page 483 - Corporate Finance PDF Final new link

P. 483

NPP

BRILLIANT’S Analysis of Risk and Uncertainty in Investment Decisions 483

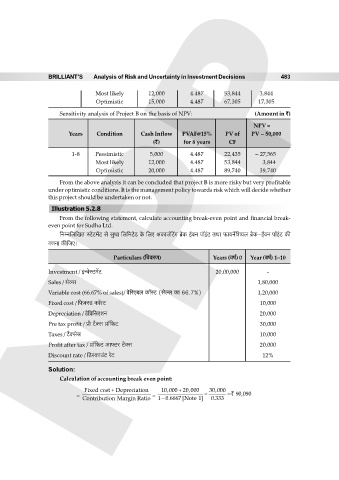

Most likely 12,000 4.487 53,844 3,844

Optimistic 15,000 4.487 67,305 17,305

Sensitivity analysis of Project B on the basis of NPV: (Amount in `)

NPV =

Years Condition Cash Inflow PVAF@15% PV of PV – 50,000

(`) for 8 years CF

1-8 Pessimistic 5,000 4.487 22,435 – 27,565

Most likely 12,000 4.487 53,844 3,844

Optimistic 20,000 4.487 89,740 39,740

From the above analysis it can be concluded that project B is more risky but very profitable

under optimistic conditions. It is the management policy towards risk which will decide whether

this project should be undertaken or not.

Illustration 5.2.8

From the following statement, calculate accounting break-even point and financial break-

even point for Sudha Ltd.

{ZåZ{b{IV ñQ>oQ>‘|Q> go gwYm {b{‘Q>oS> Ho$ {bE AH$mC§qQ>J ~«oH$ B©dZ nm°B§Q> VWm ’$m¶Z|{e¶b ~«oH$-B©dZ nm°B§Q> H$s

JUZm H$s{OE&

Particulars ({ddaU) Years (df©) 0 Year (df©) 1–10

Investment / BÝdoñQ>‘|Q> 20,00,000 -

Sales / goëg 1,80,000

Variable cost (66.67% of sales)/ do[aE~b H$m°ñQ> (goëg H$m 66.7%) 1,20,000

Fixed cost / {’$³ñS> H$m°ñQ> 10,000

Depreciation / S>o{à{gEeZ 20,000

Pre tax profit / àr Q>¡³g àm°{’$Q> 30,000

Taxes / Q>¡³gog 10,000

Profit after tax / àm°{’$Q> AmâQ>a Q>¡³g 20,000

Discount rate / {S>ñH$mC§Q> aoQ> 12%

Solution:

Calculation of accounting break even point:

Fixed cost + Depreciation 10,000 20,000 30,000

= = ` 90,090

Contribution Margin Ratio 1 0.6667 [Note 1] 0.333