Page 10 - Market Outlook Q3 2025

P. 10

www.ntda.org

10

Trailer Industry End Use Markets

of the trailer production cycle. Both data series have recently reached predicting recession resulting from a change in trade policy. Is current

cyclical peaks, in line with what has happened with the number of trade policy having a negative impact on growth? Yes it is, but, trade is

intermodal units. The same logic noted above applies to these markets. a relatively small component of the U.S. economy.

From a purely statistical perspective, the recent peak may be sending a

false signal. On the other hand, the trade policy that caused the cyclical Figure 19

expansion to stop and change trend is real.

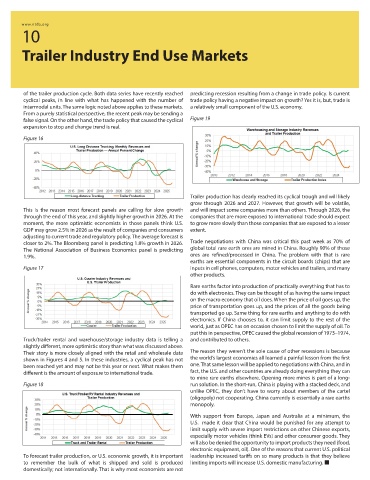

Figure 16

Trailer production has clearly reached its cyclical trough and will likely

grow through 2026 and 2027. However, that growth will be volatile,

This is the reason most forecast panels are calling for slow growth and will impact some companies more than others. Through 2026, the

through the end of this year, and slightly higher growth in 2026. At the companies that are more exposed to international trade should expect

moment, the more optimistic economists in those panels think U.S. to grow more slowly than those companies that are exposed to a lesser

GDP may grow 2.5% in 2026 as the result of companies and consumers extent.

adjusting to current trade and regulatory policy. The average forecast is

closer to 2%. The Bloomberg panel is predicting 1.8% growth in 2026. Trade negotiations with China was critical this past week as 70% of

The National Association of Business Economics panel is predicting global total rare earth ores are mined in China. Roughly 90% of those

1.9%. ores are refined/processed in China. The problem with that is rare

earths are essential components in the circuit boards (chips) that are

Figure 17 inputs in cell phones, computers, motor vehicles and trailers, and many

other products.

Rare earths factor into production of practically everything that has to

do with electronics. They can be thought of as having the same impact

on the macro economy that oil does. When the price of oil goes up, the

price of transportation goes up, and the prices of all the goods being

transported go up. Same thing for rare earths and anything to do with

electronics. If China chooses to, it can limit supply to the rest of the

world, just as OPEC has on occasion chosen to limit the supply of oil. To

put this in perspective, OPEC caused the global recession of 1973–1974,

Truck/trailer rental and warehouse/storage industry data is telling a and contributed to others.

slightly different, more optimistic story than what was discussed above.

Their story is more closely aligned with the retail and wholesale data The reason they weren’t the sole cause of other recessions is because

shown in Figures 4 and 5. In these industries, a cyclical peak has not the world’s largest economies all learned a painful lesson from the first

been reached yet and may not be this year or next. What makes them one. That same lesson will be applied to negotiations with China, and in

different is the amount of exposure to international trade. fact, the U.S. and other countries are already doing everything they can

to mine rare earths elsewhere. Opening more mines is part of a long-

Figure 18 run solution. In the short-run, China is playing with a stacked deck, and

unlike OPEC, they don’t have to worry about members of the cartel

(oligopoly) not cooperating. China currently is essentially a rare earths

monopoly.

With support from Europe, Japan and Australia at a minimum, the

U.S. made it clear that China would be punished for any attempt to

limit supply with severe import restrictions on other Chinese exports,

especially motor vehicles (think EVs) and other consumer goods. They

will also be denied the opportunity to import products they need (food,

electronic equipment, oil). One of the reasons that current U.S. political

To forecast trailer production, or U.S. economic growth, it is important leadership increased tariffs on so many products is that they believe

to remember the bulk of what is shipped and sold is produced limiting imports will increase U.S. domestic manufacturing.

domestically; not internationally. That is why most economists are not