Page 7 - FSUOGM Week 28 2022

P. 7

FSUOGM COMMENTARY FSUOGM

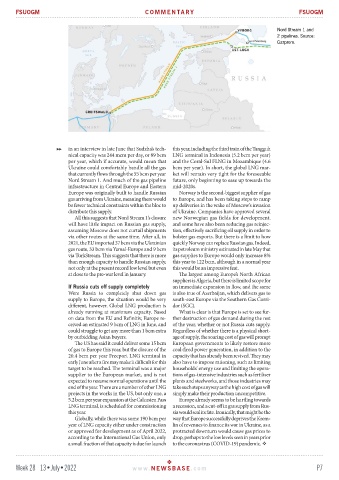

Nord Stream 1 and

2 pipelines. Source:

Gazprom.

in an interview in late June that Sudzha’s tech- this year, including the third train of the Tangguh

nical capacity was 244 mcm per day, or 89 bcm LNG terminal in Indonesia (5.2 bcm per year)

per year, which if accurate, would mean that and the Coral-Sul FLNG in Mozambique (4.6

Ukraine could comfortably handle all the gas bcm per year). In short, the global LNG mar-

that currently flows through the 55 bcm per year ket will remain very tight for the foreseeable

Nord Stream 1. And much of the gas pipeline future, only beginning to ease up towards the

infrastructure in Central Europe and Eastern mid-2020s.

Europe was originally built to handle Russian Norway is the second-biggest supplier of gas

gas arriving from Ukraine, meaning there would to Europe, and has been taking steps to ramp

be fewer technical constraints within the bloc to up deliveries in the wake of Moscow’s invasion

distribute this supply. of Ukraine. Companies have approved several

All this suggests that Nord Stream 1’s closure new Norwegian gas fields for development,

will have little impact on Russian gas supply, and some have also been reducing gas reinjec-

assuming Moscow does not curtail shipments tion, effectively sacrificing oil supply in order to

via other routes at the same time. After all, in bolster gas exports. But there is a limit to how

2021, the EU imported 37 bcm via the Ukrainian quickly Norway can replace Russian gas. Indeed,

gas route, 33 bcm via Yamal-Europe and 9 bcm its petroleum ministry estimated in late May that

via TurkStream. This suggests that there is more gas supplies to Europe would only increase 8%

than enough capacity to handle Russian supply, this year to 122 bcm, although in a normal year

not only at the present record low level but even this would be an impressive feat.

at close to the pre-war level in January. The largest among Europe’s North African

suppliers is Algeria, but there is limited scope for

If Russia cuts off supply completely an immediate expansion in flow, and the same

Were Russia to completely shut down gas is also true of Azerbaijan, which delivers gas to

supply to Europe, the situation would be very south-east Europe via the Southern Gas Corri-

different, however. Global LNG production is dor (SGC).

already running at maximum capacity. Based What is clear is that Europe is set to see fur-

on data from the EU and Refinitiv, Europe re- ther destruction of gas demand during the rest

ceived an estimated 9 bcm of LNG in June, and of the year, whether or not Russia cuts supply.

could struggle to get any more than 1 bcm extra Regardless of whether there is a physical short-

by outbidding Asian buyers. age of supply, the soaring cost of gas will prompt

The US has said it could deliver some 15 bcm European governments to likely restore more

of gas to Europe this year, but the closure of the coal-fired power generation, in addition to the

20.4 bcm per year Freeport LNG terminal in capacity that has already been revived. They may

early June after a fire may make it difficult for this also have to impose rationing, such as limiting

target to be reached. The terminal was a major households’ energy use and limiting the opera-

supplier to the European market, and is not tions of gas-intensive industries such as fertiliser

expected to resume normal operations until the plants and steelworks, and those industries may

end of the year. There are a number of other LNG take such steps anyway as the high cost of gas will

projects in the works in the US, but only one, a simply make their production uncompetitive.

5.2 bcm per year expansion at the Calcasieu Pass Europe already seems to be hurtling towards

LNG terminal, is scheduled for commissioning a recession, and a cut-off in gas supply from Rus-

this year. sia would seal its fate. Ironically, that might be the

Globally, while there was some 190 bcm per way that Europe successfully deprives the Krem-

year of LNG capacity either under construction lin of revenues to finance its war in Ukraine, as a

or approved for development as of April 2022, protracted downturn would cause gas prices to

according to the International Gas Union, only drop, perhaps to the low levels seen in years prior

a small fraction of that capacity is due for launch to the coronavirus (COVID-19) pandemic.

Week 28 13•July•2022 www. NEWSBASE .com P7