Page 7 - GLNG Week 05 2022

P. 7

GLNG COMMENTARY GLNG

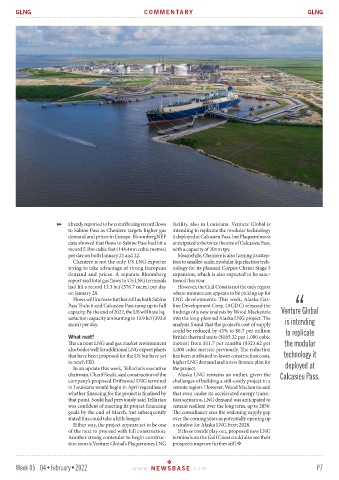

already reported to be contributing record flows facility, also in Louisiana. Venture Global is

to Sabine Pass as Cheniere targets higher gas intending to replicate the modular technology

demand and prices in Europe. BloombergNEF it deployed at Calcasieu Pass, but Plaquemines is

data showed that flows to Sabine Pass had hit a anticipated to be twice the size of Calcasieu Pass,

record 5.1bn cubic feet (144.4mn cubic metres) with a capacity of 20mn tpy.

per day on both January 21 and 22. Meanwhile, Cheniere is also turning its atten-

Cheniere is not the only US LNG exporter tion to smaller-scale, modular liquefaction tech-

trying to take advantage of strong European nology for its planned Corpus Christi Stage 3

demand and prices. A separate Bloomberg expansion, which is also expected to be sanc-

report said total gas flows to US LNG terminals tioned this year.

had hit a record 13.3 bcf (376.7 mcm) per day However, the Gulf Coast is not the only region

on January 28. where momentum appears to be picking up for

Flows will increase further still as both Sabine LNG developments. This week, Alaska Gas-

Pass Train 6 and Calcasieu Pass ramp up to full line Development Corp. (AGDC) released the

capacity. By the end of 2022, the US will have liq- findings of a new analysis by Wood Mackenzie Venture Global

uefaction capacity amounting to 13.9 bcf (393.6 into the long-planned Alaska LNG project. The

mcm) per day. analysis found that the project’s cost of supply is intending

could be reduced by 43% to $6.7 per million to replicate

What next? British thermal units ($185.32 per 1,000 cubic

The current LNG and gas market environment metres) from $11.7 per mmBtu ($323.62 per the modular

also bodes well for additional LNG export plants 1,000 cubic metres) previously. The reduction

that have been proposed for the US but have yet has been attributed to lower construction costs, technology it

to reach FID. higher LNG demand and a new finance plan for

In an update this week, Tellurian’s executive the project. deployed at

chairman, Charif Souki, said construction of the Alaska LNG remains an outlier, given the Calcasieu Pass.

company’s proposed Driftwood LNG terminal challenges of building a still-costly project in a

in Louisiana would begin in April regardless of remote region. However, Wood Mackenzie said

whether financing for the project is finalised by that even under its accelerated energy transi-

that point. Souki had previously said Tellurian tion scenarios, LNG demand was anticipated to

was confident of meeting its project financing remain resilient over the long term, up to 2050.

goals by the end of March, but subsequently The consultancy sees the widening supply gap

stated this could take a little longer. over the coming years as potentially opening up

Either way, the project appears set to be one a window for Alaska LNG from 2028.

of the next to proceed with full construction. If these trends play out, proposed new LNG

Another strong contender to begin construc- terminals on the Gulf Coast could also see their

tion soon is Venture Global’s Plaquemines LNG prospects improve further still.

Week 05 04•February•2022 www. NEWSBASE .com P7