Page 282 - Accounting Principles (A Business Perspective)

P. 282

This book is licensed under a Creative Commons Attribution 3.0 License

As briefly described in Chapter 6, to take a physical inventory, a company must count, weigh, measure, or

estimate the physical quantities of the goods on hand. For example, a clothing store may count its suits; a hardware

store may weigh bolts, washers, and nails; a gasoline company may measure gasoline in storage tanks; and a

lumberyard may estimate quantities of lumber, coal, or other bulky materials. Throughout the taking of a physical

inventory, the goal should be accuracy.

Taking a physical inventory may disrupt the normal operations of a business. Thus, the count should be

administered as quickly and as efficiently as possible. The actual taking of the inventory is not an accounting

function; however, accountants often plan and coordinate the count. Proper forms are required to record accurate

counts and determine totals. Identification names or symbols must be chosen, and those persons who count, weigh,

or measure the inventory items must know these symbols.

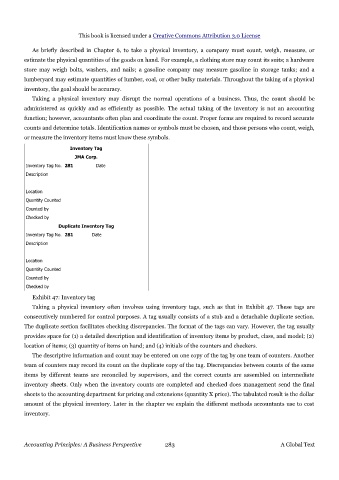

Inventory Tag

JMA Corp.

Inventory Tag No. 281 Date

Description

Location

Quantity Counted

Counted by

Checked by

Duplicate Inventory Tag

Inventory Tag No. 281 Date

Description

Location

Quantity Counted

Counted by

Checked by

Exhibit 47: Inventory tag

Taking a physical inventory often involves using inventory tags, such as that in Exhibit 47. These tags are

consecutively numbered for control purposes. A tag usually consists of a stub and a detachable duplicate section.

The duplicate section facilitates checking discrepancies. The format of the tags can vary. However, the tag usually

provides space for (1) a detailed description and identification of inventory items by product, class, and model; (2)

location of items; (3) quantity of items on hand; and (4) initials of the counters and checkers.

The descriptive information and count may be entered on one copy of the tag by one team of counters. Another

team of counters may record its count on the duplicate copy of the tag. Discrepancies between counts of the same

items by different teams are reconciled by supervisors, and the correct counts are assembled on intermediate

inventory sheets. Only when the inventory counts are completed and checked does management send the final

sheets to the accounting department for pricing and extensions (quantity X price). The tabulated result is the dollar

amount of the physical inventory. Later in the chapter we explain the different methods accountants use to cost

inventory.

Accounting Principles: A Business Perspective 283 A Global Text