Page 766 - Accounting Principles (A Business Perspective)

P. 766

This book is licensed under a Creative Commons Attribution 3.0 License

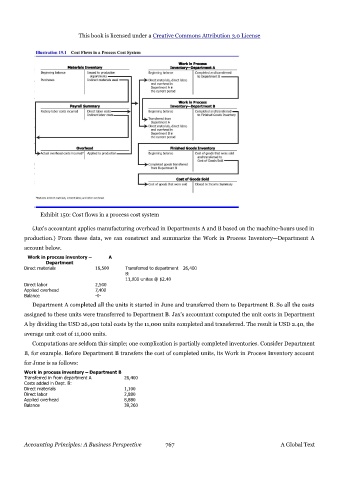

Exhibit 150: Cost flows in a process cost system

(Jax's accountant applies manufacturing overhead in Departments A and B based on the machine-hours used in

production.) From these data, we can construct and summarize the Work in Process Inventory—Department A

account below.

Work in process inventory – A

Department

Direct materials 16,500 Transferred to department 26,400

B:

11,000 unites @ $2.40

Direct labor 2,500

Applied overhead 7,400

Balance -0-

Department A completed all the units it started in June and transferred them to Department B. So all the costs

assigned to these units were transferred to Department B. Jax's accountant computed the unit costs in Department

A by dividing the USD 26,400 total costs by the 11,000 units completed and transferred. The result is USD 2.40, the

average unit cost of 11,000 units.

Computations are seldom this simple; one complication is partially completed inventories. Consider Department

B, for example. Before Department B transfers the cost of completed units, its Work in Process Inventory account

for June is as follows:

Work in process inventory – Department B

Transferred in from department A 26,400

Costs added in Dept. B:

Direct materials 1,100

Direct labor 2,880

Applied overhead 8,880

Balance 39,260

Accounting Principles: A Business Perspective 767 A Global Text