Page 829 - Accounting Principles (A Business Perspective)

P. 829

20. Using accounting for quality and cost management

of the award? If so, write a report summarizing this information. If not, search for a recent award winner that does

provide this information, and write a report summarizing the information provided.

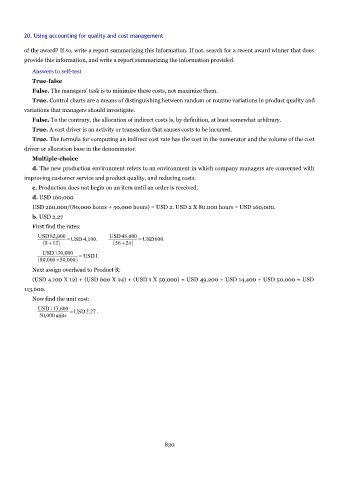

Answers to self-test

True-false

False. The managers' task is to minimize these costs, not maximize them.

True. Control charts are a means of distinguishing between random or routine variations in product quality and

variations that managers should investigate.

False. To the contrary, the allocation of indirect costs is, by definition, at least somewhat arbitrary.

True. A cost driver is an activity or transaction that causes costs to be incurred.

True. The formula for computing an indirect cost rate has the cost in the numerator and the volume of the cost

driver or allocation base in the denominator.

Multiple-choice

d. The new production environment refers to an environment in which company managers are concerned with

improving customer service and product quality, and reducing costs.

c. Production does not begin on an item until an order is received.

d. USD 160,000

USD 260,000/(80,000 hours + 50,000 hours) = USD 2. USD 2 X 80,000 hours = USD 160,000.

b. USD 2.27

First find the rates:

USD82,000 USD48,000 =USD600.

812 =USD 4,100. 5624

USD130,000 =USD1.

80,00050,000

Next assign overhead to Product R:

(USD 4,100 X 12) + (USD 600 X 24) + (USD 1 X 50,000) = USD 49,200 + USD 14,400 + USD 50,000 = USD

113,600.

Now find the unit cost:

USD113,600 =USD2.27.

50,000units

830