Page 22 - Gi August 2020

P. 22

heading for hydrogen

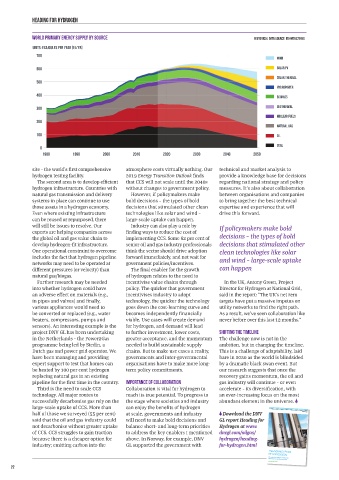

WORLD PRIMARY ENERGY SUPPLY BY SOURCE HISTORICAL DATA SOURCE: IEA WEB (2018)

UNITS: EXAJOULES PER YEAR (EJ/YR)

700

WIND

600 SOLAR PV

SOLAR THERMAL

500

HYDROPOWER

400 BIOMASS

300 GEOTHERMAL

NUCLEAR FUELS

200

NATURAL GAS

100 OIL

COAL

0

1980 1990 2000 2010 2020 2030 2040 2050

site – the world’s first comprehensive atmosphere costs virtually nothing. Our technical and market analysis to

hydrogen testing facility. 2019 Energy Transition Outlook finds provide a knowledge base for decisions

The second area is to develop efficient that CCS will not scale until the 2040s regarding national strategy and policy

hydrogen infrastructure. Countries with without changes to government policy. measures. It’s also about collaboration

natural gas transmission and delivery However, if policymakers make between organisations and companies

systems in place can continue to use bold decisions – the types of bold to bring together the best technical

those assets in a hydrogen economy. decisions that stimulated other clean expertise and experience that will

Even where existing infrastructure technologies like solar and wind – drive this forward.

can be reused or repurposed, there large-scale uptake can happen.

will still be issues to resolve. Our Industry can also play a role by If policymakers make bold

experts are helping companies across finding ways to reduce the cost of

the global oil and gas value chain to implementing CCS. Some 62 per cent of decisions – the types of bold

develop hydrogen-fit infrastructure. senior oil and gas industry professionals decisions that stimulated other

One operational constraint to overcome think the sector should drive adoption clean technologies like solar

includes the fact that hydrogen pipeline forward immediately, and not wait for and wind – large-scale uptake

networks may need to be operated at government policies/incentives.

different pressures (or velocity) than The final enabler for the growth can happen

natural gas/biogas. of hydrogen relates to the need to

Further research may be needed incentivise value chains through In the UK, Antony Green, Project

into whether hydrogen could have policy. The quicker that government Director for Hydrogen at National Grid,

an adverse effect on materials (e.g., incentivises industry to adopt said in the report: “The UK’s net zero

in pipes and valves) and finally, technology, the quicker the technology targets have put a massive impetus on

various appliances would need to goes down the cost-learning curve and utility networks to find the right path.

be converted or replaced (e.g., water becomes independently financially As a result, we’ve seen collaboration like

heaters, compressors, pumps and viable. Use cases will create demand never before over this last 12 months.”

sensors). An interesting example is the for hydrogen, and demand will lead

project DNV GL has been undertaking to further investment, lower costs, Shifting the timeline

in the Netherlands – the Power2Gas greater acceptance, and the momentum The challenge now is not in the

programme being led by Stedin, a needed to build sustainable supply ambition, but in changing the timeline.

Dutch gas and power grid operator. We chains. But to make use cases a reality, This is a challenge of adaptability, laid

have been managing and providing governments and inter-governmental bare in 2020 as the world is blindsided

expert support to test that homes can organisations have to make more long- by a dramatic black swan event. But

be heated by 100 per cent hydrogen term policy commitments. our research suggests that once the

replacing natural gas in an existing recovery gains momentum, the oil and

pipeline for the first time in the country. Importance of collaboration gas industry will continue – or even

Third is the need to scale CCS Collaboration is vital for hydrogen to accelerate – its diversification, with

technology. All major routes to reach its true potential. To progress to an ever-increasing focus on the most

successfully decarbonise gas rely on the the stage where societies and industry abundant element in the universe.

large-scale uptake of CCS. More than can enjoy the benefits of hydrogen

half of those we surveyed (55 per cent) at scale, governments and industry Download the DNV

said that the oil and gas industry could will need to make bold decisions and GL report Heading for

not decarbonise without greater uptake balance short- and long-term priorities Hydrogen at www.

of CCS. CCS struggles to gain traction to address the key enablers I mentioned dnvgl.com/oilgas/

because there is a cheaper option for above. In Norway, for example, DNV hydrogen/heading-

industry; emitting carbon into the GL supported the government with for-hydrogen.html

HEADING FOR

HYDROGEN

The oil and gas industry’s outlook for

hydrogen, from ambition to reality

SAFER, SMARTER, GREENER

22

16/07/2020 11:46

DNVGLHydrogenResearch.indd 3 16/07/2020 11:46

DNVGLHydrogenResearch.indd 3