Page 161 - Internal Auditing Standards

P. 161

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

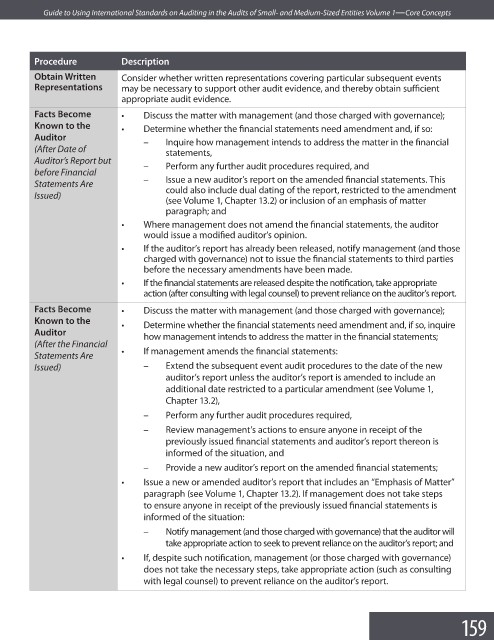

Procedure Description

Obtain Written Consider whether written representations covering particular subsequent events

Representations may be necessary to support other audit evidence, and thereby obtain suffi cient

appropriate audit evidence.

Facts Become • Discuss the matter with management (and those charged with governance);

Known to the • Determine whether the financial statements need amendment and, if so:

Auditor

– Inquire how management intends to address the matter in the fi nancial

(After Date of

statements,

Auditor’s Report but – Perform any further audit procedures required, and

before Financial

– Issue a new auditor’s report on the amended financial statements. This

Statements Are

could also include dual dating of the report, restricted to the amendment

Issued)

(see Volume 1, Chapter 13.2) or inclusion of an emphasis of matter

paragraph; and

• Where management does not amend the financial statements, the auditor

would issue a modified auditor’s opinion.

• If the auditor’s report has already been released, notify management (and those

charged with governance) not to issue the financial statements to third parties

before the necessary amendments have been made.

• If the financial statements are released despite the notification, take appropriate

action (after consulting with legal counsel) to prevent reliance on the auditor’s report.

Facts Become • Discuss the matter with management (and those charged with governance);

Known to the

• Determine whether the financial statements need amendment and, if so, inquire

Auditor

how management intends to address the matter in the fi nancial statements;

(After the Financial

Statements Are • If management amends the fi nancial statements:

Issued) – Extend the subsequent event audit procedures to the date of the new

auditor’s report unless the auditor’s report is amended to include an

additional date restricted to a particular amendment (see Volume 1,

Chapter 13.2),

– Perform any further audit procedures required,

– Review management’s actions to ensure anyone in receipt of the

previously issued financial statements and auditor’s report thereon is

informed of the situation, and

– Provide a new auditor’s report on the amended fi nancial statements;

• Issue a new or amended auditor’s report that includes an “Emphasis of Matter”

paragraph (see Volume 1, Chapter 13.2). If management does not take steps

to ensure anyone in receipt of the previously issued financial statements is

informed of the situation:

– Notify management (and those charged with governance) that the auditor will

take appropriate action to seek to prevent reliance on the auditor’s report; and

• If, despite such notification, management (or those charged with governance)

does not take the necessary steps, take appropriate action (such as consulting

with legal counsel) to prevent reliance on the auditor’s report.

159