Page 593 - ITGC_Audit Guides

P. 593

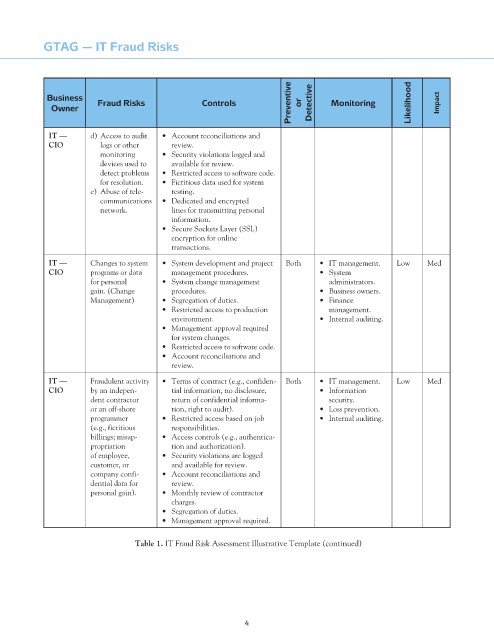

GTAG — IT Fraud Risks

Preventive or Detective Monitoring Likelihood Impact

Business

Controls

Fraud Risks

Owner

it — d) Access to audit • Account reconciliations and

cio logs or other review.

monitoring • Security violations logged and

devices used to available for review.

detect problems • Restricted access to software code.

for resolution. • Fictitious data used for system

e) Abuse of tele- testing.

communications • Dedicated and encrypted

network. lines for transmitting personal

information.

• Secure Sockets Layer (SSL)

encryption for online

transactions.

it — Changes to system • System development and project Both • IT management. Low Med

cio programs or data management procedures. • System

for personal • System change management administrators.

gain. (Change procedures. • Business owners.

Management) • Segregation of duties. • Finance

• Restricted access to production management.

environment. • Internal auditing.

• Management approval required

for system changes.

• Restricted access to software code.

• Account reconciliations and

review.

it — Fraudulent activity • Terms of contract (e.g., confiden- Both • IT management. Low Med

cio by an indepen- tial information, no disclosure, • Information

dent contractor return of confidential informa- security.

or an off-shore tion, right to audit). • Loss prevention.

programmer • Restricted access based on job • Internal auditing.

(e.g., fictitious responsibilities.

billings; misap- • Access controls (e.g., authentica-

propriation tion and authorization).

of employee, • Security violations are logged

customer, or and available for review.

company confi- • Account reconciliations and

dential data for review.

personal gain). • Monthly review of contractor

charges.

• Segregation of duties.

• Management approval required.

table 1. IT Fraud Risk Assessment Illustrative Template (continued)

4