Page 44 - IRS Employer Tax Forms

P. 44

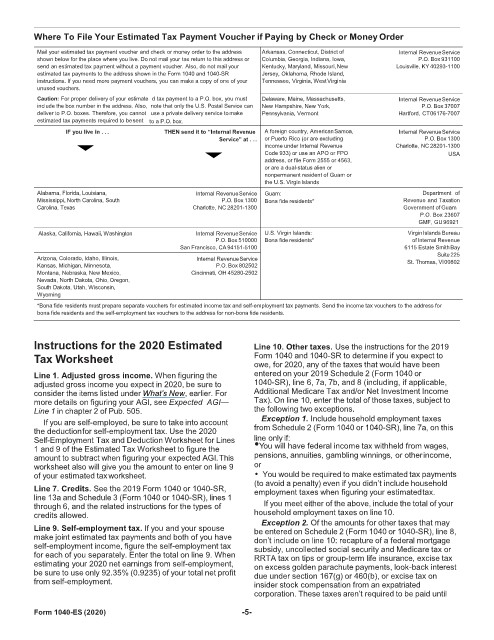

Where To File Your Estimated Tax Payment Voucher if Paying by Check or Money Order

Mail your estimated tax payment voucher and check or money order to the address Arkansas, Connecticut, District of Internal RevenueService

shown below for the place where you live. Do not mail your tax return to this address or Columbia, Georgia, Indiana, Iowa, P.O. Box 931100

send an estimated tax payment without a payment voucher. Also, do not mail your Kentucky, Maryland, Missouri,New Louisville, KY 40293-1100

estimated tax payments to the address shown in the Form 1040 and 1040-SR Jersey, Oklahoma, Rhode Island,

instructions. If you need more payment vouchers, you can make a copy of one of your Tennessee, Virginia, WestVirginia

unused vouchers.

Caution: For proper delivery of your estimate d tax payment to a P.O. box, you must Delaware, Maine, Massachusetts, Internal RevenueService

include the box number in the address. Also, note that only the U.S. Postal Service can New Hampshire, New York, P.O. Box 37007

deliver to P.O. boxes. Therefore, you cannot use a private delivery service tomake Pennsylvania, Vermont Hartford, CT06176-7007

estimated tax payments required to besent to a P.O. box.

IF you live in . . . THEN send it to “Internal Revenue A foreign country, AmericanSamoa, Internal RevenueService

Service” at . .. or Puerto Rico (or are excluding P.O. Box 1300

income under Internal Revenue Charlotte, NC 28201-1300

Code 933) or use an APO or FPO USA

address, or file Form 2555 or 4563,

or are a dual-status alien or

nonpermanent resident of Guam or

the U.S. VirginIslands

Alabama, Florida, Louisiana, Internal RevenueService Guam: Department of

Mississippi, North Carolina, South P.O. Box 1300 Bona fide residents* Revenue and Taxation

Carolina, Texas Charlotte, NC 28201-1300 Government of Guam

P.O. Box 23607

GMF, GU96921

Alaska, California, Hawaii, Washington Internal RevenueService U.S. Virgin Islands: Virgin Islands Bureau

P.O. Box 510000 Bona fide residents* of Internal Revenue

San Francisco, CA 94151-5100 6115 Estate SmithBay

Suite225

Arizona, Colorado, Idaho, Illinois, Internal RevenueService St. Thomas, VI00802

Kansas, Michigan, Minnesota, P.O. Box 802502

Montana, Nebraska, New Mexico, Cincinnati, OH 45280-2502

Nevada, North Dakota, Ohio, Oregon,

South Dakota, Utah, Wisconsin,

Wyoming

*Bona fide residents must prepare separate vouchers for estimated income tax and self-employment tax payments. Send the income tax vouchers to the address for

bona fide residents and the self-employment tax vouchers to the address for non-bona fide residents.

Instructions for the 2020 Estimated Line 10. Other taxes. Use the instructions for the 2019

Tax Worksheet Form 1040 and 1040-SR to determine if you expect to

owe, for 2020, any of the taxes that would have been

Line 1. Adjusted gross income. When figuring the entered on your 2019 Schedule 2 (Form 1040 or

adjusted gross income you expect in 2020, be sure to 1040-SR), line 6, 7a, 7b, and 8 (including, if applicable,

consider the items listed under What’s New, earlier. For Additional Medicare Tax and/or Net Investment Income

more details on figuring your AGI, see Expected AGI— Tax). On line 10, enter the total of those taxes, subject to

Line 1 in chapter 2 of Pub. 505. the following two exceptions.

If you are self-employed, be sure to take into account Exception 1. Include household employment taxes

the deductionfor self-employment tax. Use the 2020 from Schedule 2 (Form 1040 or 1040-SR), line 7a, on this

Self-Employment Tax and Deduction Worksheet for Lines line only if:

1 and 9 of the Estimated Tax Worksheet to figure the •You will have federal income tax withheld from wages,

amount to subtract when figuring your expected AGI.This pensions, annuities, gambling winnings, or otherincome,

worksheet also will give you the amount to enter on line 9 or

of your estimated taxworksheet. • You would be required to make estimated tax payments

Line 7. Credits. See the 2019 Form 1040 or 1040-SR, (to avoid a penalty) even if you didn’t include household

employment taxes when figuring your estimatedtax.

line 13a and Schedule 3 (Form 1040 or 1040-SR), lines 1

through 6, and the related instructions for the types of If you meet either of the above, include the total of your

credits allowed. household employment taxes on line10.

Exception 2. Of the amounts for other taxes that may

Line 9. Self-employment tax. If you and your spouse be entered on Schedule 2 (Form 1040 or 1040-SR), line 8,

make joint estimated tax payments and both of you have don’t include on line 10: recapture of a federal mortgage

self-employment income, figure the self-employment tax subsidy, uncollected social security and Medicare tax or

for each of you separately. Enter the total on line 9. When RRTA tax on tips or group-term life insurance, excise tax

estimating your 2020 net earnings from self-employment, on excess golden parachute payments, look-back interest

be sure to use only 92.35% (0.9235) of your total net profit due under section 167(g) or 460(b), or excise tax on

from self-employment. insider stock compensation from an expatriated

corporation. These taxes aren’t required to be paid until

Form 1040-ES (2020) -5-