Page 340 - Large Business IRS Training Guides

P. 340

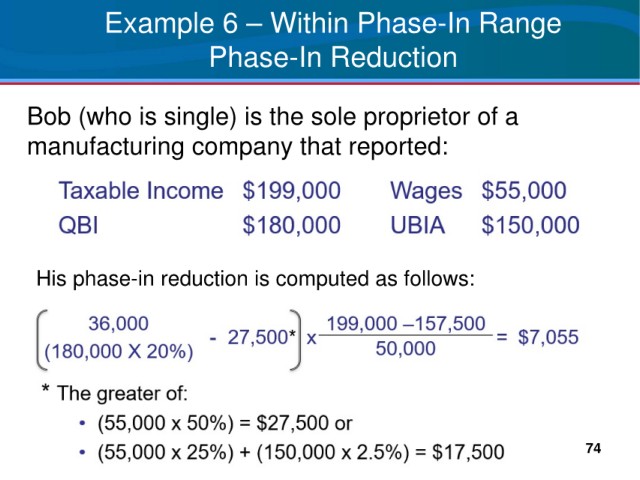

Example 6 – Within Phase-In Range

Phase-In Reduction

Bob (who is single) is the sole proprietor of a

manufacturing company that reported:

His phase-in reduction is computed as follows:

74