Page 21 - Supplement to Income Tax 2020

P. 21

Additions & Corrections to the Text of Your Income Tax 2020

No technical correction for qualified improvement IRS interest rate for first quarter of 2020 (pages 782,

property glitch (pages 739, 741). The new law does not 787). For January-March 2020, the IRS interest rate for

include a correction to the drafting error in the Tax Cuts individual taxpayer refunds and underpayments is 5%,

and Jobs Act that failed to reduce the recovery period the same as for the third and fourth quarters of 2019. The

for qualified improvement property to 15 years, as 5% rate applicable in March also applies for purposes of

had been intended. As a result, qualified improvement figuring any estimated tax penalty due for the first 15 days

property remains subject to a 39-year recovery period, of April; this is so even if the IRS rate for the April 1-June

and it is not eligible for bonus depreciation. 30 quarter is lower (or much less likely, higher) than 5%.

Auto depreciation safe harbor if bonus depreciation Minimum penalty for late filing (page 782). Under the

claimed (page 748). Under “Deductions for later years SECURE Act, the minimum penalty for filing a return

in the recovery period,” the text “Caution” should read late by more than 60 days is increased to the lesser of

as follows: “Under the safe harbor, depreciation for $435 (up from $330) or 100% of the tax due. This

years two through six is the lesser of (1) the MACRS applies to 2019 returns due in 2020. The $435 amount

rate from Table 43-4 or Table 43-5, whichever applies, may be increased for inflation for years after 2020.

multiplied by the basis that remains after the first year,

or (2) the annual depreciation ceiling for the year from IRS authority to charge fees for PTINs (page 991 of

Table 43-2 or Table 43-3.” Professional Edition). The Supreme Court declined

to hear an appeal by a group of tax return preparers

Refund claim for bad debt or worthless security

(page 785). The second paragraph of 47.2 should from a D.C. Circuit decision (Montrois v. United States,

read as follows: “A refund claim based on a bad debt 916 F.3d 1056) that upheld the authority of the IRS

or worthless securities may be made within seven to charge tax return preparers a fee for obtaining and

years of the original due date of the return (without renewing a PTIN. (The IRS has not charged a fee for

extensions) for the year in which the debt or security PTINs for the 2020 tax filing season.)

became worthless.”

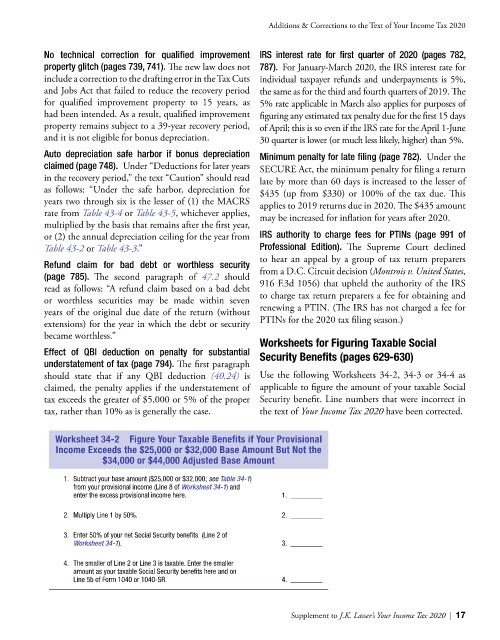

Worksheets for Figuring Taxable Social

Effect of QBI deduction on penalty for substantial Security Benefits (pages 629-630)

understatement of tax (page 794). The first paragraph

should state that if any QBI deduction (40.24) is Use the following Worksheets 34-2, 34-3 or 34-4 as

claimed, the penalty applies if the understatement of applicable to figure the amount of your taxable Social

tax exceeds the greater of $5,000 or 5% of the proper Security benefit. Line numbers that were incorrect in

tax, rather than 10% as is generally the case. the text of Your Income Tax 2020 have been corrected.

Worksheet 34-2 Figure Your Taxable Benefits if Your Provisional

Income Exceeds the $25,000 or $32,000 Base Amount But Not the

$34,000 or $44,000 Adjusted Base Amount

1. Subtract your base amount ($25,000 or $32,000; see Table 34-1)

from your provisional income (Line 8 of Worksheet 34-1) and

enter the excess provisional income here. 1.

2. Multiply Line 1 by 50%. 2.

3. Enter 50% of your net Social Security benefits (Line 2 of

Worksheet 34-1). 3.

4. The smaller of Line 2 or Line 3 is taxable. Enter the smaller

amount as your taxable Social Security benefits here and on

Line 5b of Form 1040 or 1040-SR. 4.

Supplement to J.K. Lasser’s Your Income Tax 2020 | 17