Page 233 - ic92 actuarial

P. 233

Foundations of Casualty Actuarial Science

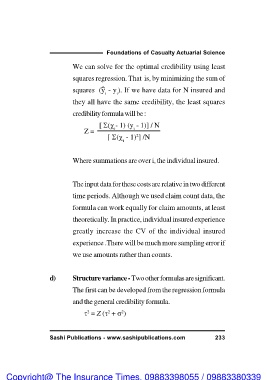

We can solve for the optimal credibility using least

squares regression. That is, by minimizing the sum of

squares (yi - yi). If we have data for N insured and

they all have the same credibility, the least squares

credibility formula will be :

Z = [ (i- 1) (yi - 1)] / N

[ (i - 1)2] /N

Where summations are over i, the individual insured.

The input data for these costs are relative in two different

time periods. Although we used claim count data, the

formula can work equally for claim amounts, at least

theoretically. In practice, individual insured experience

greatly increase the CV of the individual insured

experience .There will be much more sampling error if

we use amounts rather than counts.

d) Structure variance - Two other formulas are significant.

The first can be developed from the regression formula

and the general credibility formula.

2 = Z (2 + 2)

Sashi Publications - www.sashipublications.com 233

Copyright@ The Insurance Times. 09883398055 / 09883380339