Page 187 - IC46 addendum

P. 187

Indian Accounting Standards

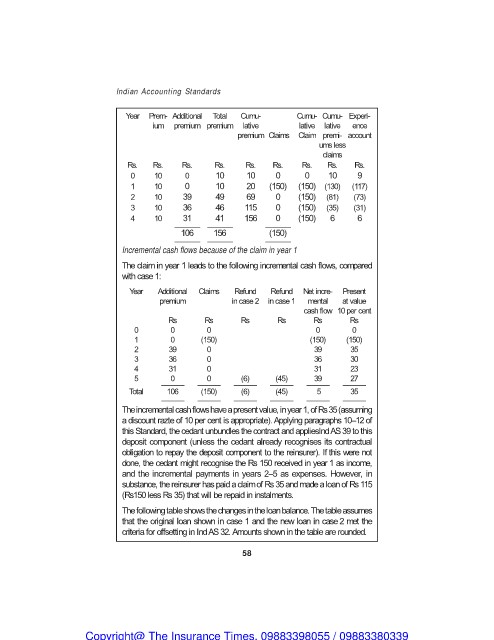

Year Prem- Additional Total Cumu- Cumu- Cumu- Experi-

ium premium premium lative lative lative ence

premium Claims Claim premi- account

ums less

claims

Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs. Rs.

0 10 0 10 10 0 0 10 9

1 10 0

10 20 (150) (150) (130) (117)

2 10 39 49 69 0 (150) (81) (73)

3 10 36 46 115 0 (150) (35) (31)

4 10 ___3_1__ __4_1___ 156 ___0___ (150) 6 6

__1_0_6__ __1_5_6__ _(_1_5_0_)_

Incremental cash flows because of the claim in year 1

The claim in year 1 leads to the following incremental cash flows, compared

with case 1:

Year Additional Claims Refund Refund Net incre- Present

premium in case 2 in case 1 mental at value

cash flow 10 per cent

Rs Rs Rs Rs Rs Rs

000 00

1 0 (150) (150) (150)

2 39 0 39 35

3 36 0 36 30

4 31 0 31 23

5 ___0___ ___0___ __(_6_)__ __(_4_5_) _ ___39___ ___2_7__

Total __1_0_6__ _(_1_5_0_)_ __(_6_)__ __(_4_5_) _ ___5___ ___3_5__

The incremental cash flows have a present value, in year 1, of Rs 35 (assuming

a discount razte of 10 per cent is appropriate). Applying paragraphs 10–12 of

this Standard, the cedant unbundles the contract and appliesInd AS 39 to this

deposit component (unless the cedant already recognises its contractual

obligation to repay the deposit component to the reinsurer). If this were not

done, the cedant might recognise the Rs 150 received in year 1 as income,

and the incremental payments in years 2–5 as expenses. However, in

substance, the reinsurer has paid a claim of Rs 35 and made a loan of Rs 115

(Rs150 less Rs 35) that will be repaid in instalments.

The following table shows the changes in the loan balance. The table assumes

that the original loan shown in case 1 and the new loan in case 2 met the

criteria for offsetting in Ind AS 32. Amounts shown in the table are rounded.

58

Copyright@ The Insurance Times. 09883398055 / 09883380339