Page 408 - Introduction to Business

P. 408

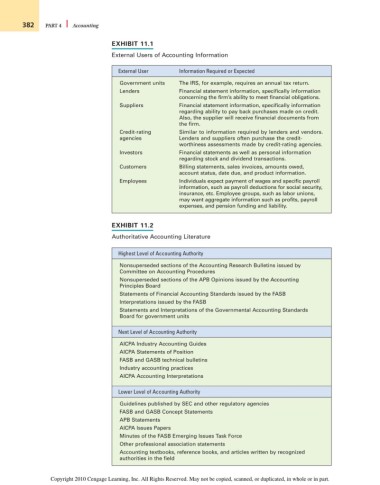

382 PART 4 Accounting

EXHIBIT 11.1

External Users of Accounting Information

External User Information Required or Expected

Government units The IRS, for example, requires an annual tax return.

Lenders Financial statement information, specifically information

concerning the firm’s ability to meet financial obligations.

Suppliers Financial statement information, specifically information

regarding ability to pay back purchases made on credit.

Also, the supplier will receive financial documents from

the firm.

Credit-rating Similar to information required by lenders and vendors.

agencies Lenders and suppliers often purchase the credit-

worthiness assessments made by credit-rating agencies.

Investors Financial statements as well as personal information

regarding stock and dividend transactions.

Customers Billing statements, sales invoices, amounts owed,

account status, date due, and product information.

Employees Individuals expect payment of wages and specific payroll

information, such as payroll deductions for social security,

insurance, etc. Employee groups, such as labor unions,

may want aggregate information such as profits, payroll

expenses, and pension funding and liability.

EXHIBIT 11.2

Authoritative Accounting Literature

Highest Level of Accounting Authority

Nonsuperseded sections of the Accounting Research Bulletins issued by

Committee on Accounting Procedures

Nonsuperseded sections of the APB Opinions issued by the Accounting

Principles Board

Statements of Financial Accounting Standards issued by the FASB

Interpretations issued by the FASB

Statements and Interpretations of the Governmental Accounting Standards

Board for government units

Next Level of Accounting Authority

AICPA Industry Accounting Guides

AICPA Statements of Position

FASB and GASB technical bulletins

Industry accounting practices

AICPA Accounting Interpretations

Lower Level of Accounting Authority

Guidelines published by SEC and other regulatory agencies

FASB and GASB Concept Statements

APB Statements

AICPA Issues Papers

Minutes of the FASB Emerging Issues Task Force

Other professional association statements

Accounting textbooks, reference books, and articles written by recognized

authorities in the field

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.