Page 410 - Introduction to Business

P. 410

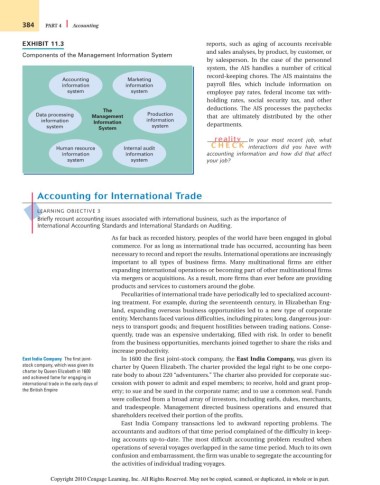

384 PART 4 Accounting

EXHIBIT 11.3 reports, such as aging of accounts receivable

and sales analyses, by product, by customer, or

Components of the Management Information System

by salesperson. In the case of the personnel

system, the AIS handles a number of critical

record-keeping chores. The AIS maintains the

Accounting Marketing

information information payroll files, which include information on

system system employee pay rates, federal income tax with-

holding rates, social security tax, and other

deductions. The AIS processes the paychecks

The

Data processing Management Production that are ultimately distributed by the other

information Information information

system System system departments.

reality In your most recent job, what

CH ECK

Human resource Internal audit interactions did you have with

information information accounting information and how did that affect

system system your job?

Accounting for International Trade

LEARNING OBJECTIVE 3

Briefly recount accounting issues associated with international business, such as the importance of

International Accounting Standards and International Standards on Auditing.

As far back as recorded history, peoples of the world have been engaged in global

commerce. For as long as international trade has occurred, accounting has been

necessary to record and report the results. International operations are increasingly

important to all types of business firms. Many multinational firms are either

expanding international operations or becoming part of other multinational firms

via mergers or acquisitions. As a result, more firms than ever before are providing

products and services to customers around the globe.

Peculiarities of international trade have periodically led to specialized account-

ing treatment. For example, during the seventeenth century, in Elizabethan Eng-

land, expanding overseas business opportunities led to a new type of corporate

entity. Merchants faced various difficulties, including pirates; long, dangerous jour-

neys to transport goods; and frequent hostilities between trading nations. Conse-

quently, trade was an expensive undertaking, filled with risk. In order to benefit

from the business opportunities, merchants joined together to share the risks and

increase productivity.

East India Company The first joint- In 1600 the first joint-stock company, the East India Company, was given its

stock company, which was given its charter by Queen Elizabeth. The charter provided the legal right to be one corpo-

charter by Queen Elizabeth in 1600

and achieved fame for engaging in rate body to about 220 “adventurers.” The charter also provided for corporate suc-

international trade in the early days of cession with power to admit and expel members; to receive, hold and grant prop-

the British Empire erty; to sue and be sued in the corporate name; and to use a common seal. Funds

were collected from a broad array of investors, including earls, dukes, merchants,

and tradespeople. Management directed business operations and ensured that

shareholders received their portion of the profits.

East India Company transactions led to awkward reporting problems. The

accountants and auditors of that time period complained of the difficulty in keep-

ing accounts up-to-date. The most difficult accounting problem resulted when

operations of several voyages overlapped in the same time period. Much to its own

confusion and embarrassment, the firm was unable to segregate the accounting for

the activities of individual trading voyages.

Copyright 2010 Cengage Learning, Inc. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part.