Page 223 - AAA Integrated Workbook STUDENT S18-J19

P. 223

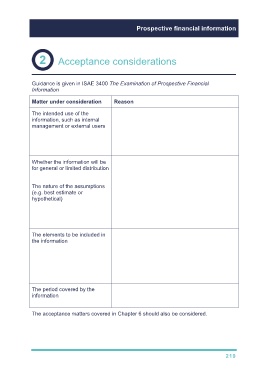

Prospective financial information

Acceptance considerations

Guidance is given in ISAE 3400 The Examination of Prospective Financial

Information

Matter under consideration Reason

The intended use of the Information for external use will be relied upon by

information, such as internal third parties, potentially for making investment

management or external users decisions.

This makes it riskier for the accountant because

the consequences of inappropriate reports will be

more severe.

Whether the information will be Information for general distribution will potentially

for general or limited distribution result in the assignment being higher risk as a

larger audience will be relying on it.

The nature of the assumptions If information is best-estimate, it should be a

(e.g. best estimate or reasonable approximation as to what might

hypothetical) actually happen therefore lower risk.

Where the assumptions are hypothetical, they will

be more difficult to validate and therefore higher

risk.

The elements to be included in The engagement will be higher risk if the PFI

the information includes elements of which the accountant has

little knowledge or that are extremely complex or

highly subjective.

The external auditor is likely to have the greatest

understanding of the entity therefore would be best

placed to provide this service.

The period covered by the Short-term forecasts are likely to be more easily

information verified than projections looking out over a longer

period therefore less risky.

The acceptance matters covered in Chapter 6 should also be considered.

219