Page 93 - AAA Integrated Workbook STUDENT S18-J19

P. 93

Planning, materiality and assessing the risk of material misstatement

Audit strategy and plan

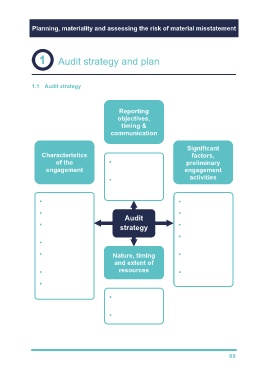

1.1 Audit strategy

Reporting

objectives,

timing &

communication

Significant

Characteristics factors,

of the Timetable for preliminary

engagement reporting engagement

Communication activities

with client, team

& 3 parties

rd

FR framework Materiality

Industry reporting Risk assessment

Audit

Knowledge of strategy Internal controls

business

Need for

Internal audit scepticism

Service Nature, timing Changes in laws

organisation and extent of & regulations

Use of CAATs resources Significant

developments

Availability of

client staff

Selection of audit

team

Budget

89